So, you’ve been dreaming of that perfect home in the US, right? Maybe it’s a cozy bungalow in Florida, a bustling city apartment in New York, or a sprawling ranch in Texas. Whatever your vision, there’s a crucial step that stands between you and those keys: the mortgage pre-approval process. And let me tell you, this isn’t just some bureaucratic hurdle; it’s your golden ticket, your secret weapon in a competitive housing market . But here’s the thing: many people dive in without truly understanding what it entails, and that can lead to unnecessary stress, delays, or even a missed opportunity. That’s why I’m here to guide you through it, like a friend who’s navigated these waters before, sharing the insider tips you won’t always find in a basic search.

Let’s be honest, the world of home buying can feel overwhelming, especially when you’re dealing with finances in a new country or simply trying to get ahead in a fast-paced environment. But getting your mortgage pre-approval sorted early can transform your home search from a hopeful dream into a concrete plan. It tells sellers you’re serious, financially capable, and ready to close the deal. Think of it as getting your VIP pass before the concert – you know you’re getting in, and you can focus on enjoying the show (or, in this case, finding your dream home).

Pre-Qualification vs. Pre-Approval | Knowing the Difference

Before we dive deep, let’s clear up a common confusion: `mortgage pre-qualification` versus `mortgage pre-approval`. Many folks use these terms interchangeably, but they are distinctly different, and understanding this distinction is vital.

Pre-qualification is often a quick, informal estimate. You provide a `loan officer` with some basic financial information – income, debts, assets – and they give you a ballpark figure of how much you might be able to borrow. It usually doesn’t involve a credit check, and it’s more of a self-assessment or a soft inquiry. It’s useful for getting a general idea, but it doesn’t carry much weight with sellers.

Now, `mortgage pre-approval`? That’s the real deal. This is where a lender actually reviews your financial history in detail. They pull your credit report, verify your income and employment, and assess your assets and debts. The result is a formal `pre-approval letter`, stating the exact loan amount they are willing to lend you, often with an estimated interest rate. This letter is a powerful tool. It shows sellers you’re not just window shopping; you’re a qualified buyer, and that can make all the difference in a multiple-offer situation in the competitive US real estate market.

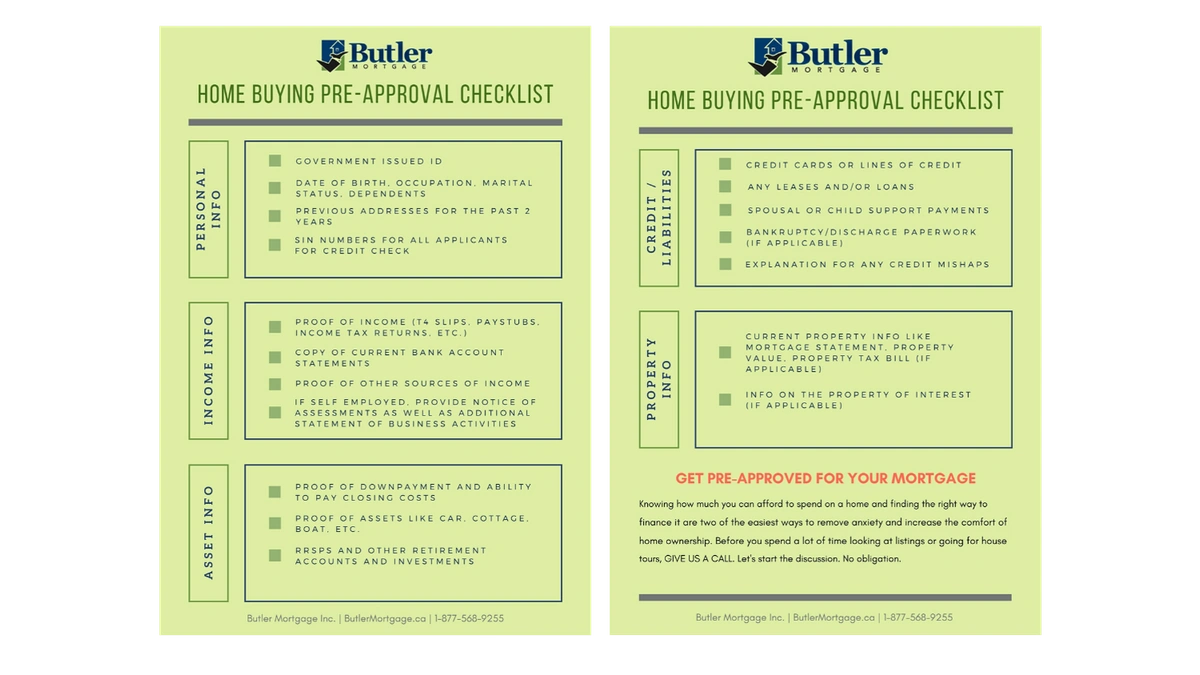

The Essential Checklist | What Lenders Really Look For

When you seek mortgage pre-approval, lenders are essentially trying to gauge your risk. They want to know you’re a reliable borrower who can consistently make payments. So, what exactly are they scrutinizing? Here’s the rundown:

Your Credit Score | The Foundation

This is paramount. Your credit score is a numerical representation of your creditworthiness. Lenders use it to predict how likely you are to repay your `home loan`. Generally, the higher your score, the better interest rates you’ll qualify for. While `credit score requirements` vary by loan type and lender, aiming for a score above 700 is always a good strategy for securing favorable terms. A common mistake I see people make is not checking their credit report before applying. Do it! Dispute any errors you find.

Income and Employment Stability | Your Earning Power

Lenders want to see a steady, reliable income. They’ll typically ask for at least two years of employment history, verifying your job stability. This means providing pay stubs, W-2 forms, and sometimes even letters from your employer. If you’re self-employed, you’ll need two years of tax returns and profit and loss statements. They’re looking for consistency, which is a strong indicator of your ability to manage a long-term financial commitment like a home loan.

Assets and Debts | Your Financial Health Snapshot

This is where your overall financial health comes into play. Lenders will examine your assets (savings accounts, checking accounts, investment accounts) to ensure you have enough for a down payment and `closing costs`, plus reserves. Equally important is your `debt-to-income ratio` (DTI). This ratio compares your monthly debt payments to your gross monthly income. Most lenders prefer a DTI of 36% or less, though it can go higher depending on other factors. High DTI can be a red flag, so it’s wise to pay down credit card balances or other loans before applying.

Gathering Your Financial Documents | Be Prepared!

To verify all the above, you’ll need to provide a stack of `financial documents`. This can feel like a lot, but having them ready makes the process smooth. Expect to provide:

- Recent pay stubs (30-60 days)

- Bank statements (last 2-3 months)

- Tax returns (last two years)

- W-2 forms (last two years)

- Statements for any other assets (investment accounts, retirement funds)

- Proof of identity (driver’s license, passport)

Navigating the Application | Your Journey with a Loan Officer

Once you have your documents in order, the next step is to engage with a `loan officer`. This person will be your primary contact throughout the pre-approval and ultimately, the loan application process. Finding the right one is crucial. Don’t just go with the first `mortgage lenders USA` you find; shop around, compare services, and read reviews. A good loan officer will explain everything clearly and answer all your questions.

During the application, you’ll formally submit all your `financial documents`. The lender will then perform a ‘hard inquiry’ on your credit score, which will temporarily ding it by a few points. Don’t panic; this is normal. The key is to do all your rate shopping within a short period (typically 14-45 days, depending on the scoring model) so multiple inquiries count as one for scoring purposes. This shows you’re serious about finding the best terms for your home loan.

Receiving Your Pre-Approval Letter | Now What?

Congratulations! You’ve received your `pre-approval letter`. This document is gold. It will clearly state the maximum loan amount you’re approved for, often with an estimated interest rate and the type of loan. It will also have an expiration date, usually 60-90 days, so keep an eye on that. If it expires, you’ll need to update your documentation and get re-approved.

With this letter in hand, you are now a confident, empowered buyer in the housing market. When you find a home you love, you can present your offer with the `pre-approval letter`, signaling to the seller that you are a serious and capable buyer. This can give you a significant advantage over buyers who are only pre-qualified or haven’t done their homework yet. It streamlines the entire process, making your offer more attractive and reducing the chances of the deal falling through due to financing issues. Remember, while this letter is a strong indication, it’s not a final loan commitment. The final approval comes after the property appraisal and a complete underwriting review.

Frequently Asked Questions About Mortgage Pre-Approval

What if my credit score isn’t perfect?

Don’t despair! While a higher credit score is ideal, many `mortgage lenders USA` offer programs for individuals with less-than-perfect credit. You might qualify for an FHA loan, for example, which has lower `credit score requirements`. The best approach is to speak with a `loan officer` who can assess your situation and advise on steps to improve your score or suitable loan options. Sometimes, waiting a few months to boost your score can save you thousands in interest over the life of the loan.

How long does a mortgage pre-approval last?

Typically, a mortgage pre-approval is valid for 60 to 90 days. The reason for this limited timeframe is that your financial situation can change. Lenders want to ensure the information they based their approval on is still accurate. If your `pre-approval letter` is nearing its expiration date and you haven’t found a home yet, you’ll need to contact your lender to update your financial information and get a renewed `pre-approval letter`.

Does pre-approval guarantee a loan?

No, a `pre-approval letter` does not guarantee a loan. It’s a conditional commitment based on the information you provided and the lender’s initial assessment of your creditworthiness. The final approval is contingent on several factors, including a satisfactory appraisal of the property you choose, a thorough review of all your `financial documents` by the underwriting department, and no significant changes to your financial health or employment status. It’s a very strong indicator, but not the final word.

Can I get pre-approved by multiple lenders?

Yes, and it’s actually recommended! Shopping around with different lenders allows you to compare interest rates, fees, and terms. As mentioned earlier, if you do this within a focused period (e.g., 14-45 days), multiple hard inquiries for a home loan will typically be treated as a single inquiry on your credit score, minimizing the impact. This strategy can lead to significant savings over the life of your mortgage. For general financial advice and tools, you can also check out resources like the Consumer Financial Protection Bureau .

What documents needed for mortgage pre approval?

To reiterate, you’ll generally need recent pay stubs, bank statements, tax returns (last two years), W-2 forms (last two years), and statements for any other assets or debts. Having these `financial documents` organized and ready before you start the process will make it much smoother and faster. Think of it as preparing your homework before the class starts!

Is there a cost of mortgage pre approval?

In most cases, getting mortgage pre-approval itself doesn’t come with a direct fee. However, some lenders might charge a small fee for pulling your credit report, though this is often waived or credited back if you proceed with them for your `home loan`. Any costs associated with the loan, such as appraisal fees or origination fees, typically come later in the actual loan application and closing process, not during the initial pre-approval stage. It’s always best to ask your `loan officer` about any potential costs upfront.

Understanding the mortgage pre-approval process USA isn’t just about ticking boxes; it’s about empowering yourself in one of the biggest financial decisions of your life. It’s about being prepared, confident, and strategic. By taking the time to gather your `financial documents`, understand your credit score, and work closely with a trusted `loan officer`, you’re not just getting a piece of paper; you’re setting yourself up for success in finding and securing your dream home. Don’t underestimate its power – it’s your first, most vital step towards homeownership. And if you’re exploring other financial avenues, remember that a solid financial plan is always key, whether it’s for a home loan or any other loan . Happy house hunting!