Alright, let’s talk cars. Specifically, that often-dreaded, sometimes-confusing part of buying one: the car loan down payment requirements USA . You’re probably picturing a big chunk of cash, right? Maybe you’re wondering if you really need one, or how much is enough, or perhaps you’ve heard whispers of a magical no down payment car loan . Here’s the thing: while it might feel like a hurdle, understanding down payments is actually your secret weapon to a smoother, smarter car buying experience in the States. And let me tell you, it’s not as complex as some make it out to be.

I’ve seen countless folks navigate this maze, and what fascinates me is how a little knowledge can save you thousands. This isn’t just about handing over money; it’s about setting yourself up for financial success. So, grab a coffee, and let’s dive deep into the world of auto financing. We’ll explore not just the “what,” but the “why” and, crucially, the “how” to make your down payment work for you.

Why a Down Payment Matters (Beyond Just Lowering Monthly Payments)

You might think a down payment’s only job is to reduce your monthly outgo, and yes, it absolutely does that. But that’s just scratching the surface. A substantial down payment is like telling the lender, “Hey, I’m serious about this car, and I’m a responsible borrower.” This message carries a lot of weight, especially when it comes to securing favorable terms on your auto loan .

First off, it reduces your loan-to-value (LTV) ratio. In plain English? It means you’re borrowing less relative to the car’s worth. This makes you a less risky borrower in the eyes of the bank. Less risk often translates directly into lower car loan interest rates . Over the life of a five or six-year loan, even a percentage point or two can save you hundreds, if not thousands, of dollars. Think about that: a bit more upfront can mean significantly less overall cost.

Then there’s the immediate equity. Cars depreciate, and they do it fast – sometimes losing 10-20% of their value the moment you drive them off the lot. If you put down a healthy down payment, you’re less likely to be “underwater” on your loan, meaning you owe more than the car is worth. This is a common mistake I see people make, and it can be a real headache if you need to sell or trade in your car sooner than expected. It’s about protecting your investment from day one.

And let’s not forget the credit score impact. While a down payment doesn’t directly boost your score, it can enable you to get approved for better loan terms, which can then positively reflect on your credit history if you make timely payments. Lenders are more willing to work with you when you show financial commitment.

So, How Much Do You Really Need? The ‘Minimum Down Payment for Car’ Demystified

This is probably the million-dollar question, isn’t it? The truth is, there’s no single, universally mandated minimum down payment for car across the board in the USA. However, industry standards and lender preferences definitely exist. Generally speaking, for a new vehicle, a 10-20% down payment is often recommended, and for a used car loan , it can be higher, sometimes 15-25%.

Why the difference? New cars tend to hold their value better initially, and lenders might feel more secure withnew car financing. Used cars, on the other hand, have already taken a depreciation hit and might be older, making them a slightly riskier asset for the lender. That said, this isn’t a hard and fast rule. Some lenders might approve you with less, especially if you have an excellent credit score.

What about those aggressive offers you see? You know, the “zero down payment!” ads? We’ll get to those in a bit. But for now, understand that a car dealership down payment expectation often hovers around these percentages. It gives them confidence, and it gives you a stronger negotiating position. It’s a win-win, really.

Cracking the Code | Factors Influencing Your Down Payment

Alright, so we know the general guidelines. But what specifically dictates how much you might need, or how much you should put down? It’s a blend of several key factors:

Your Credit Score | The Big Player

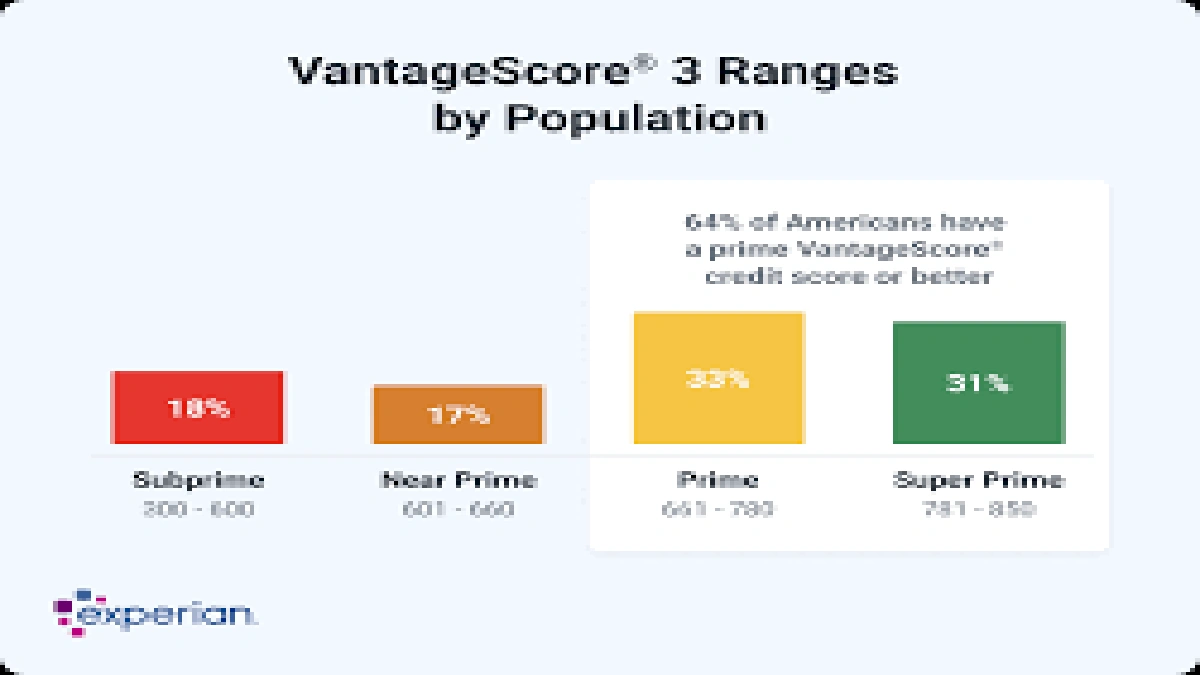

This is perhaps the most significant factor. If you have a stellar credit score (think 700+), lenders might be more flexible with their down payment requirements, sometimes even offering low or zero down payment options if you qualify. Why? Because your credit history demonstrates a strong ability to manage debt responsibly. Conversely, if your credit score is on the lower side, a larger down payment becomes even more crucial. It acts as a buffer for the lender, mitigating their risk.

Vehicle Type | New vs. Used, Luxury vs. Economy

As I touched on earlier, a new car financing deal might have slightly lower implied down payment expectations than a used car loan . Luxury vehicles, due to their higher price tags and potentially faster depreciation curves (in terms of absolute dollar value), might also warrant a larger down payment to keep the loan-to-value ratio in check. An economy sedan will likely have different parameters than a high-end SUV.

Lender Policies | Not All Banks Are Created Equal

Each bank, credit union, and financial institution has its own underwriting criteria. Some lenders are more conservative, while others are more aggressive. It’s why shopping around for your loan is just as important as shopping for the car itself. Don’t just take the first offer! A smaller, local credit union might have more flexible terms than a large national bank, or vice-versa, depending on their current lending goals. This is a great area to explore forbest personal loan lenders USA 2026, as their offerings can sometimes provide alternative financing routes.

Loan Term | The Length of Your Commitment

A longer loan term (say, 72 or 84 months) might tempt you with lower monthly payments, but it also means you’re paying more interest over time and potentially staying underwater on your loan for longer. Lenders might prefer a larger down payment on longer terms to offset this extended risk. Shorter terms (36 or 48 months) often come with more lenient down payment expectations because the loan is paid off quicker.

The Holy Grail | Can You Get a ‘No Down Payment Car Loan’ in the USA?

Ah, the allure of the no down payment car loan ! It sounds fantastic, doesn’t it? Drive off the lot with no money down. And yes, they absolutely exist in the USA. But here’s the analyst in me coming out: they’re not always the “holy grail” they appear to be.

These loans are typically reserved for buyers with excellent credit scores, strong income, and a very low debt-to-income ratio. Lenders see you as such a safe bet that they’re willing to take on the entire risk. However, even for these prime borrowers, there are often trade-offs. You’ll likely face higher monthly payments because you’re financing the entire cost of the vehicle. And, as we discussed, you’ll immediately be underwater on your loan due to depreciation.

For those with less-than-perfect credit, a zero-down option is usually a red flag. It often comes with significantly higher car loan interest rates , extended loan terms, and a higher total cost over the life of the loan. While it might provideinstant liquidity, the long-term financial implications can be substantial.

My advice? Approach “no down payment” offers with a healthy dose of skepticism. Always read the fine print, calculate the total cost, and compare it against scenarios where you do put some money down. Sometimes, the immediate gratification isn’t worth the long-term financial burden.

Smart Strategies for Your Car Loan Down Payment | Practical Auto Loan Tips

So, what’s the smart play here? How do you prepare for or optimize your car loan down payment ? It’s all about strategy and preparation.

- Start Saving Early: This might seem obvious, but it’s the most effective strategy. Even a small amount saved consistently can add up. Set a target percentage (10-20% of your target car price) and work towards it.

- Consider Your Trade-In: If you have an existing vehicle, its trade-in value can significantly contribute to, or even cover, your down payment. Get a fair appraisal from multiple sources (dealerships, online tools like Kelley Blue Book or Edmunds) before you negotiate.

- Sell Your Old Car Privately: Often, selling your car yourself can fetch a higher price than trading it in at a dealership. This extra cash can then go directly towards your new car’s down payment. It requires more effort, but the financial reward can be worth it.

- Negotiate the Price of the Car: Remember, the down payment is a percentage of the car’s price. If you can negotiate a lower purchase price for the vehicle, you effectively reduce the amount needed for your down payment. Every dollar saved on the car’s price is a dollar less you need to put down (or finance).

- Explore All Financing Options: Don’t just rely on the dealership’s financing. Get pre-approved with your bank or credit union before you even step foot on the lot. This gives you leverage and a benchmark interest rate. Sometimes, considering a personal loan for a portion of the down payment, if your credit is good, can be an option, but be mindful of the interest rates on personal loans, which can sometimes be higher than auto loans. For more insights on lenders, you might want to check out resources like the Consumer Financial Protection Bureau’s auto loan guide.

- Use a down payment calculator: Many online tools can help you visualize how different down payment amounts affect your monthly payments and total interest paid. This can be incredibly empowering for planning your purchase.

Frequently Asked Questions About Car Loan Down Payments

What’s the typical down payment percentage for a car loan in the USA?

While there’s no strict rule, most financial experts and lenders recommend putting down at least 10-20% for a new car and 15-25% for a used car. This helps reduce your monthly payments, lowers the total interest paid, and helps you avoid being “underwater” on your loan.

Does a larger down payment always mean a better deal on my auto loan?

Generally, yes! A larger down payment reduces the amount you need to borrow, which typically leads to lower monthly payments and can help you qualify for lower car loan interest rates . It also gives you more equity in the vehicle from the start, which is a smart financial move.

Can I use my trade-in as a down payment for a new car?

Absolutely! Using your existing vehicle as a trade-in is a very common and effective way to cover all or part of your down payment. The trade-in value is directly applied to the purchase price of your new car, reducing the amount you need to finance.

What if I have bad credit? How does that affect my down payment?

If you have bad credit, a larger down payment becomes even more critical. Lenders view you as a higher risk, so a substantial down payment acts as a safeguard for them. It increases your chances of approval and can slightly offset the higher car loan interest rates you might face due to a lower credit score .

Are there programs for first-time car buyers with low down payments?

Some dealerships or manufacturers occasionally offer special incentives or programs for first-time buyers, which might include lower down payment options. However, these often come with specific eligibility criteria or slightly higher interest rates. It’s always best to research and compare these offers carefully.

How can I estimate how much down payment I need?

You can use an onlinedown payment calculator. Input the car’s price, your desired loan term, and an estimated interest rate. Then, adjust the down payment amount to see how it impacts your monthly payment and total cost. This helps you plan your budget effectively.

So there you have it. Understanding car loan down payment requirements USA isn’t just about ticking a box; it’s about empowering yourself to make one of the biggest purchases most people make with confidence and intelligence. By taking the time to understand these factors and adopting smart strategies, you’re not just buying a car; you’re investing in your financial well-being. Drive smart, my friend!