Okay, let’s be honest. The world of student loans can feel like navigating a dense jungle, right? You’re trying to fund your education, chase your dreams, and suddenly you’re drowning in jargon like ‘subsidized,’ ‘unsubsidized,’ ‘variable rates,’ and ‘origination fees.’ It’s enough to make anyone’s head spin. But here’s the thing: understanding the fundamental difference between federal student loans and private student loans isn’t just about picking a financial product. It’s about setting the stage for your financial future, potentially for decades. And trust me, the why behind this choice is far more crucial than most people realize.

I’ve seen countless students dive into their education funding without truly grasping the profound implications of this distinction. It’s not just a comparison; it’s a strategic decision that can either offer you a robust safety net during tough times or leave you exposed. So, let’s pull back the curtain on this vital student loan comparison USA and uncover why your choice here is perhaps the most significant financial decision you’ll make before you even graduate.

Understanding the Players | Federal Student Loans

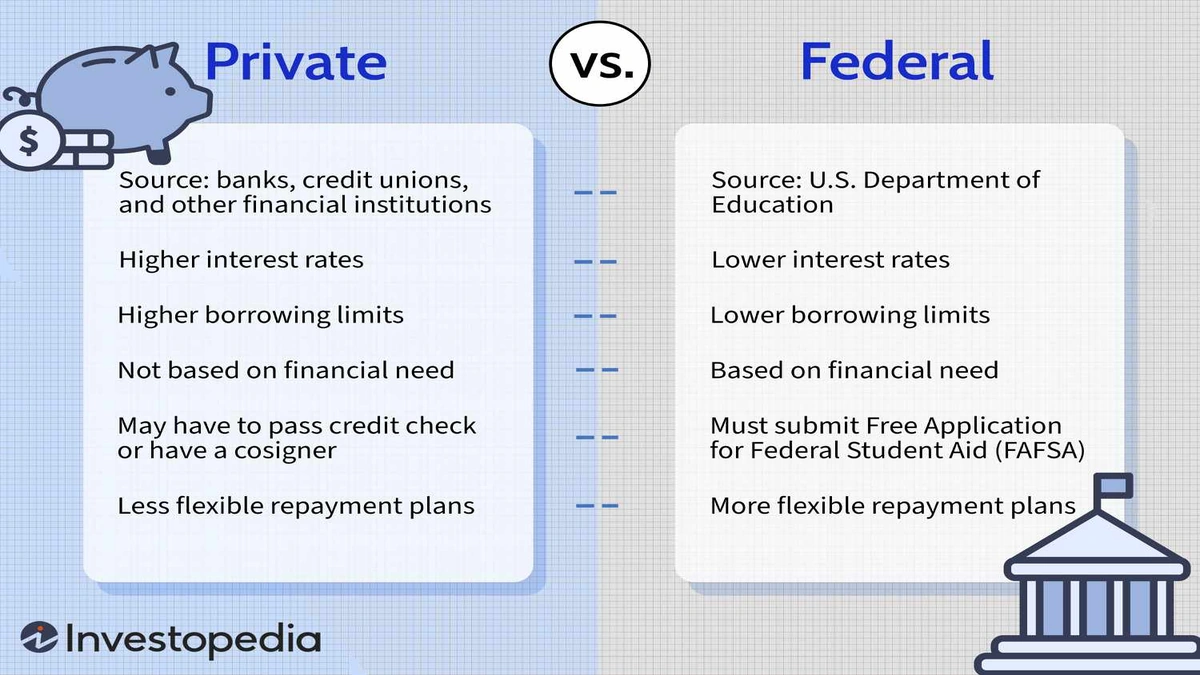

Think of federal student loans as the government’s way of saying, “We believe in your education, and we’re going to give you a fair shot.” These loans are funded by the U.S. government and come with a suite of benefits designed to protect borrowers. When you fill out thatFAFSA application, you’re essentially applying for access to these very loans.

The Perks | Why Federal Loans Often Win

What fascinates me about federal loans is their inherent borrower-friendliness. Unlike private options, these aren’t solely based on your (or your co-signer’s) credit score requirements . Instead, they often come with fixed student loan interest rates , meaning your rate won’t suddenly jump up, even if the market gets volatile. This predictability is a huge comfort.

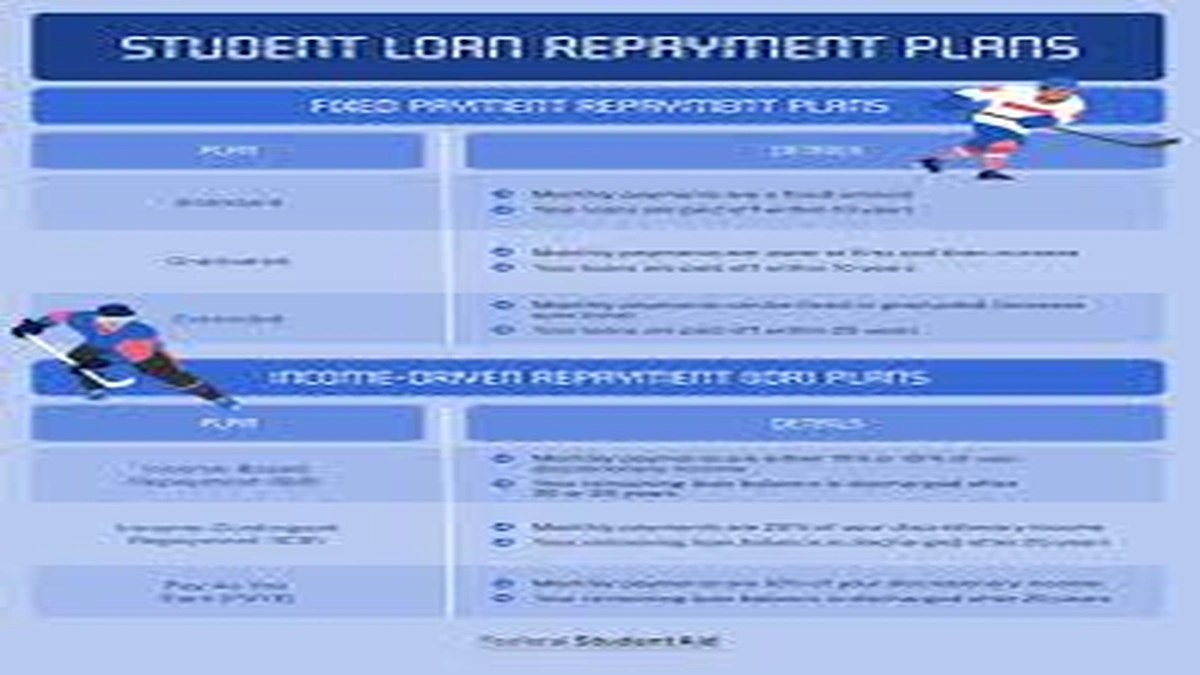

But the real game-changer lies in their repayment options . We’re talking about income-driven repayment (IDR) plans, where your monthly payment is adjusted based on your income and family size. Imagine losing your job or facing an unexpected medical bill – with federal loans, you have options like deferment or forbearance that can temporarily pause your payments. This flexibility is a lifeline, not just a feature. And for those entering public service, there are even loan forgiveness programs like Public Service Loan Forgiveness (PSLF), which can wipe out remaining balances after a certain number of qualifying payments. This isn’t just a benefit; it’s a profound social safety net built into the system.

Another often-overlooked perk? The grace period . After you graduate or drop below half-time enrollment, you typically get a six-month grace period before you have to start making payments. This gives you crucial time to land a job and get your finances in order without immediate pressure.

Stepping into the Private Arena | Private Student Loans

Now, let’s talk about private student loans . These are offered by banks, credit unions, and other financial institutions. They’re essentially personal loans specifically for education. While they fill a crucial gap when federal aid isn’t enough, they operate on a very different philosophy: profit.

The Pitfalls | When Private Loans Become Tricky

The first thing to understand about private loans is that they are credit-based. This means your eligibility and your interest rates are heavily dependent on your (or your co-signer’s) creditworthiness. If you’re a young student with little to no credit history, you’ll almost certainly need a co-signer, and even then, your rate might be higher than you’d like. What’s more, these rates can be fixed or variable, and variable rates can be a real wild card, potentially increasing your monthly payments significantly over time.

Private loans generally lack the robust borrower protections found in federal loans. Forget about income-driven repayment plans or widespread loan forgiveness programs . While some private lenders might offer limited deferment or forbearance options, they are typically less generous and harder to qualify for. The moment you face financial hardship, your options are far more limited. This is a critical distinction, especially when considering long-term student debt management.

I often advise students to exhaust all federal options, including grants, scholarships, and federal loans, before even glancing at private loan offerings. The difference in borrower protections is simply too vast to ignore. It’s like choosing between walking a tightrope with a safety net versus walking it without one.

The Great Divide | Key Differences That Impact You

Understanding the fundamental nature of these student loan types is just the beginning. Let’s really dig into the core differences that will directly affect your wallet and your peace of mind.

Interest Rates | A Crucial Variable

Federal loans, as mentioned, typically offer fixed student loan interest rates that are often lower than private loan rates, especially for borrowers with less-than-stellar credit. These rates are set by Congress and are usually the same for all borrowers, regardless of credit score. Private loan rates, however, are dynamic. They can be fixed or variable, and they’re heavily influenced by market conditions and your credit profile. A variable rate might start low, but it could climb over the life of the loan, making your monthly payments unpredictable and potentially much higher. This is a huge risk factor that needs careful consideration when evaluating any student loan application process .

Repayment Options & Flexibility | Your Safety Net

This is where federal loans truly shine. Beyond the standard repayment, they offer a host of income-driven plans (PAYE, REPAYE, IBR, ICR) that adjust your payments based on your income. This can be a lifesaver during periods of unemployment or low income. They also offer deferment (postponing payments for specific reasons like going back to school) and forbearance (temporarily pausing payments due to financial hardship). Private lenders, on the other hand, offer far fewer and less generous options. If you hit a rough patch, you’re largely on your own, facing potentially severe consequences if you can’t make your payments. This flexibility is a prime example of federal loan benefits over private loan drawbacks .

Loan Forgiveness & Protections | What’s Really There?

Federal loans come with built-in borrower protections. Beyond income-driven repayment leading to potential forgiveness after 20-25 years, programs like PSLF offer forgiveness for those in public service. There are also provisions for loan discharge in cases of total and permanent disability, or if your school closes. Private loans offer virtually none of these protections. If you’re looking for genuine loan forgiveness programs , you’ll almost exclusively find them in the federal sphere. This difference is stark and represents a significant risk when you’re understanding loan terms from private lenders.

Making Your Move | How to Decide

So, how do you navigate this? The strategy is clear: prioritize. Always, always, always start with federal student aid. Fill out the FAFSA, explore all grants and scholarships you qualify for, and then consider federal loans. Only after exhausting those options should you even think about private loans. If you do need private funding, shop around, compare student loan interest rates diligently, and understand every single term. Look for lenders with some level of hardship assistance, even if it’s limited. And remember, you can alwaysexplore various loan optionsto ensure you’re making the most informed choice.

It’s also crucial to remember that your choice isn’t necessarily permanent. While less flexible for private loans, refinancing student loans is an option down the line. You can refinance federal loans into a private loan (though you’d lose federal protections), or consolidate multiple federal loans. This is a complex area, and it’s worth understanding the implications ofunderstanding processing feesand terms for any refinancing decision.

FAQs | Your Burning Questions Answered

What’s the absolute first step I should take for student loans?

The absolute first step is to complete the Free Application for Federal Student Aid (FAFSA). This form determines your eligibility for federal grants, scholarships, and federal student loans. Do this every year you plan to attend school.

Can I have both federal and private student loans?

Yes, it’s common for students to have a mix of both. Typically, students max out their federal loan eligibility first, and if there’s still a funding gap, they turn to private loans to cover the remaining costs.

Is a co-signer always required for private student loans?

Not always, but often. If you have a limited credit history or a low credit score, a co-signer with good credit will significantly increase your chances of approval and help you secure a lower interest rate . It’s one of the common credit score requirements .

What happens if I can’t pay my student loans?

For federal loans, you have many options like income-driven repayment plans, deferment, or forbearance. For private loans, options are far more limited. Defaulting on either can severely damage your credit score and lead to collections, wage garnishment, and other serious consequences.

Are federal student loan interest rates always lower than private ones?

While federal loan interest rates are often lower and fixed, it’s not a universal rule. A private loan borrower with excellent credit and a strong co-signer might qualify for a lower variable rate than some federal loan options. However, this is rare, and the trade-off is losing federal protections.

What’s the difference between subsidized and unsubsidized federal loans?

Subsidized loans are based on financial need, and the government pays the interest while you’re in school at least half-time, during your grace period , and during deferment. Unsubsidized loans are not need-based, and interest accrues from the moment the loan is disbursed, even while you’re in school. It’s a key distinction in understanding loan terms .

The Bottom Line | Beyond the Numbers

Choosing between federal vs private student loans comparison USA isn’t just a simple calculation; it’s about evaluating risk, understanding your future financial flexibility, and leveraging the protections available to you. Federal loans, with their fixed rates, income-driven repayment options , and potential loan forgiveness programs , offer a buffer against life’s uncertainties. Private loans, while necessary for some, come with fewer safety nets and demand a higher degree of personal financial discipline and stability.

My advice? Approach this decision with the same seriousness you would a major investment. Don’t just look at the initial interest rate; look at the entire ecosystem of benefits and drawbacks. Your financial well-being post-graduation hinges on this choice. Make it wisely.