Alright, let’s talk mortgages. Specifically, the age-old dilemma that keeps many potential homeowners in the USA up at night: fixed vs adjustable mortgage rates USA . It’s not just a financial decision; it’s a long-term commitment, a gamble on the future, and frankly, a bit of a headache if you don’t know what you’re getting into. As someone who’s seen countless people navigate this maze, let me tell you, there’s no one-size-fits-all answer. But what I can do is arm you with the knowledge and the right questions to ask yourself, so you can make a choice that truly fits your life.

Here’s the thing: understanding these two fundamental mortgage options is crucial. It’s not about picking the “better” one, but the “better for you ” one. And that, my friend, depends entirely on your financial situation, your risk tolerance, and even your gut feeling about the future of the US housing market and interest rates. So, grab a coffee, and let’s break it down, step-by-step.

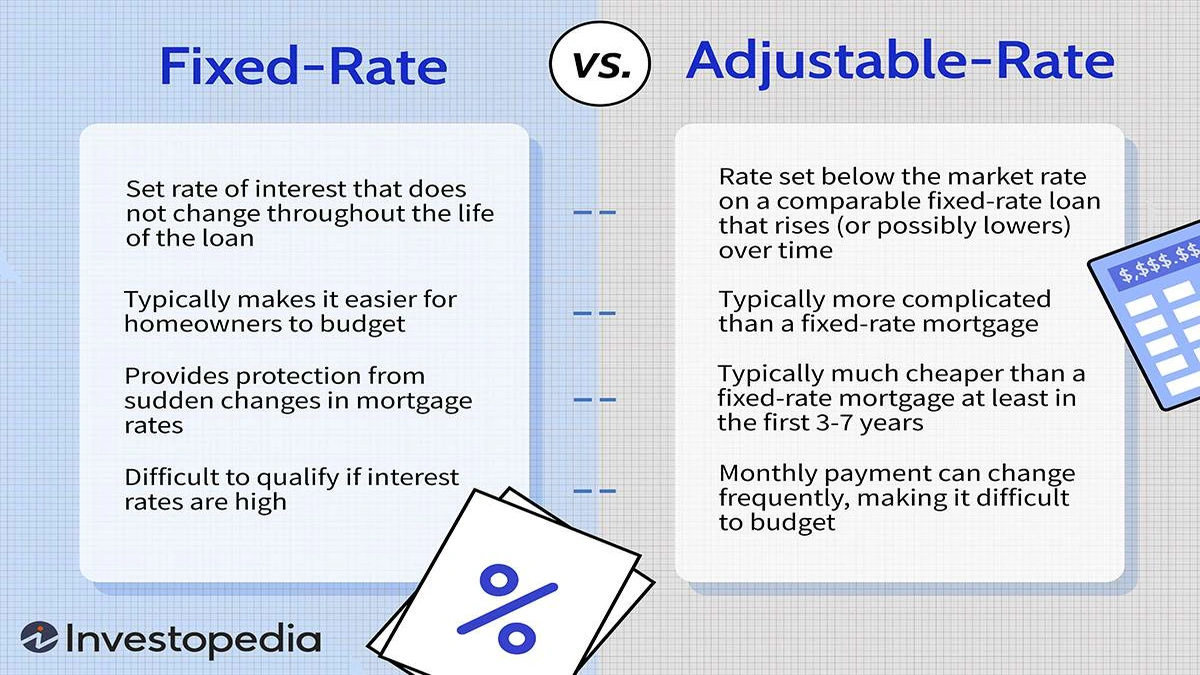

Decoding Fixed-Rate Mortgages | The Predictable Path

Imagine knowing exactly what your biggest monthly expense will be for the next 15, 20, or even 30 years. That’s the core promise of a fixed mortgage rate . Your interest rate, and consequently your monthly payments , stay the same from day one until you pay off the loan. Period. No surprises, no sudden jumps, just steady, predictable budgeting. It’s like having a financial comfort blanket.

This predictability is a huge draw, especially for those who value payment stability above all. If you’re planning to stay in your home for a long time, or if you simply can’t stomach the idea of your housing costs fluctuating, then a fixed-rate mortgage often feels like the safest harbor. You lock in today’s rate, and even if market rates soar in five years, yours remains untouched. This peace of mind, for many, is priceless.

But let’s be honest, nothing in finance is without its trade-offs. The flip side? If interest rates drop significantly, you won’t automatically benefit. You’d have to go through the process of refinancing options to secure a lower rate, which comes with its own costs and paperwork. So, while it offers security, it might also mean missing out on potential savings if the market moves in your favor. It’s a classic low-risk, potentially lower-reward scenario.

Unpacking Adjustable-Rate Mortgages (ARMs) | The Dynamic Choice

Now, let’s talk about the more adventurous sibling: the adjustable mortgage rates , commonly known as ARM loans . Unlike their fixed counterparts, ARMs start with an initial, typically lower, interest rate that is fixed for a certain period say, 3, 5, 7, or 10 years. After this initial period, the rate adjusts periodically (usually annually) based on a specified market index, plus a margin set by your lender.

What fascinates me about ARMs is their initial allure. That lower starting rate can make a significant difference in your initial monthly payments , potentially allowing you to qualify for a larger loan or simply free up cash flow in the early years. This can be incredibly attractive, especially if you’re a specific borrower profile perhaps someone who anticipates a significant income increase, plans to sell the home within the initial fixed period, or expects interest rates to fall.

However, this is where the plot thickens. The “adjustable” part means your payments can go up or down. While there are usually caps on how much the rate can change in a single adjustment period and over the life of the loan, the potential for increased interest rate risk is very real. If market rates skyrocket, so could your monthly outlay, sometimes significantly. I’ve seen people caught off guard by these adjustments, which can strain budgets that were once comfortable.

So, why would anyone choose an ARM? Well, if you’re confident you’ll sell or refinance before the fixed period ends, or if you genuinely believe mortgage market trends are heading towards lower rates, an ARM could be a strategic play. It’s a calculated risk, offering potential short-term savings for long-term uncertainty.

Making Your Choice | A Step-by-Step Guide

Okay, so how do you decide between these two beasts? It’s not about which one is inherently “better,” but which one aligns with your unique situation. Here’s how I advise people to think through it:

1. Assess Your Time Horizon | How Long Will You Stay?

This is perhaps the most critical question. If you envision staying in your home for less than 5-7 years, an ARM might be worth considering. The initial fixed period often aligns perfectly with shorter-term plans, allowing you to benefit from the lower introductory rate without facing the adjustment risks. But if this is your “forever home,” or at least a 10+ year commitment, the stability of fixed mortgage rates usually wins out.

2. Evaluate Your Risk Tolerance | Can You Handle the Unknown?

Are you someone who thrives on predictability, or do you have a higher tolerance for financial fluctuations? If the thought of your mortgage payment potentially increasing gives you anxiety, a fixed rate is your friend. If you’re comfortable with the idea of market shifts and have a robust emergency fund to absorb potential payment hikes, an ARM might not seem as daunting. Think about your personal comfort level with interest rate stability .

3. Consider Your Financial Future | Income & Growth

Do you anticipate significant income growth in the coming years? If you’re early in your career and expect substantial raises, an ARM’s potential payment increases might be less of a concern. Conversely, if your income is stable or you’re nearing retirement, the certainty of a fixed payment becomes even more appealing. It’s about aligning your loan terms with your expected earning trajectory.

4. Analyze Market Expectations: What Are the Housing Market Predictions ?

This is where things get a bit speculative, but it’s still important. What are the general forecasts for interest rates? If experts widely predict rates to fall, an ARM might be more attractive. If they’re expected to rise, a fixed rate locks in a potentially lower rate now. Remember, no one has a crystal ball, but staying informed about economic indicators can provide valuable context. This is also where financial planning for mortgages comes into play.

5. Crunch the Numbers | Don’t Guess, Calculate!

Use online mortgage calculators to compare initial payments, potential future payments (for ARMs, consider worst-case scenarios with rate caps), and total interest paid over the life of both types of loans. Don’t just look at the starting rate; calculate the total cost. This due diligence is paramount. A common mistake I see people make is only focusing on the initial monthly payment without understanding the long-term implications.

The Refinancing Factor | A Strategic Move

It’s important to remember that your initial choice isn’t necessarily set in stone forever. Many homeowners consider refinancing options down the line. If you choose a fixed rate and rates drop significantly, you might refinance into a new, lower fixed rate. If you have an ARM and rates start to climb uncomfortably, you might refinance into a fixed rate to lock in stability. However, refinancing comes with closing costs, so it’s a strategy to be used judiciously, not as a guaranteed escape hatch.

The Bottom Line | Your Mortgage, Your Future

Ultimately, choosing between fixed vs adjustable mortgage rates USA is a deeply personal decision. It requires a hard look at your current finances, your future plans, and your comfort with risk. There’s no magic bullet, only informed choices. By taking the time to understand the nuances, considering your personal circumstances, and doing your homework, you can confidently select the mortgage options that will serve you best on your path to homeownership. Don’t let anyone rush you; this is one of the biggest financial decisions you’ll ever make. Choose wisely, my friend.

Frequently Asked Questions About Mortgage Rates

What is the main difference between fixed and adjustable mortgage rates?

The core difference lies in the interest rate’s stability. A fixed mortgage rate remains constant throughout the loan term, providing predictable monthly payments . An adjustable mortgage rate (ARM) starts with a fixed rate for an initial period, after which it adjusts periodically based on market indices, leading to fluctuating payments.

Are ARM loans always riskier than fixed-rate mortgages?

Generally, yes, ARM loans carry more interest rate risk due to the uncertainty of future payments. However, for borrowers with specific financial strategies or short-term homeownership plans, the initial lower rate of an ARM can be advantageous. The risk depends heavily on individual circumstances and market conditions.

When is a fixed-rate mortgage a better choice?

A fixed mortgage rate is often a better choice if you plan to stay in your home for a long time (typically 7+ years), prioritize payment stability and predictability, or if current mortgage market trends suggest interest rates are likely to rise in the future. It offers peace of mind against market fluctuations.

Can I convert an adjustable-rate mortgage to a fixed-rate mortgage?

Yes, it’s often possible to convert an ARM to a fixed-rate mortgage through refinancing options . This involves taking out a new fixed-rate loan to pay off your existing ARM. It’s a common strategy if interest rates start to climb or if your financial situation changes, but it does involve closing costs.

How do I know what my adjustable rate will change to?

Your ARM loan documents will specify the index (e.g., SOFR, CMT) your rate is tied to, the margin added by your lender, and the adjustment frequency. They will also outline initial, periodic, and lifetime caps on how much your interest rate can increase. While you can’t predict the exact future index value, these caps provide a limit to your potential payment increases.