Alright, let’s be honest. When you’re looking at a gold loan , the initial relief of gettinginstant liquidityis fantastic. It’s a lifesaver for many, offering quick cash against an asset sitting idle in your locker. But here’s the thing: that initial ‘yay!’ often overshadows the crucial part – how you actually pay it back. And believe me, just like a well-played cricket match, strategy is everything when it comes to managing your gold loan repayment options .

I’ve seen countless individuals dive into gold loans without truly understanding the nuances of their repayment choices. It’s not just about paying an EMI; it’s about picking a plan that aligns with your unique financial rhythm, your cash flow, and your long-term goals. Getting this wrong can turn a helpful financial tool into a source of unnecessary stress. So, let’s pull back the curtain and explain these options, making sure you’re equipped to make the smartest move.

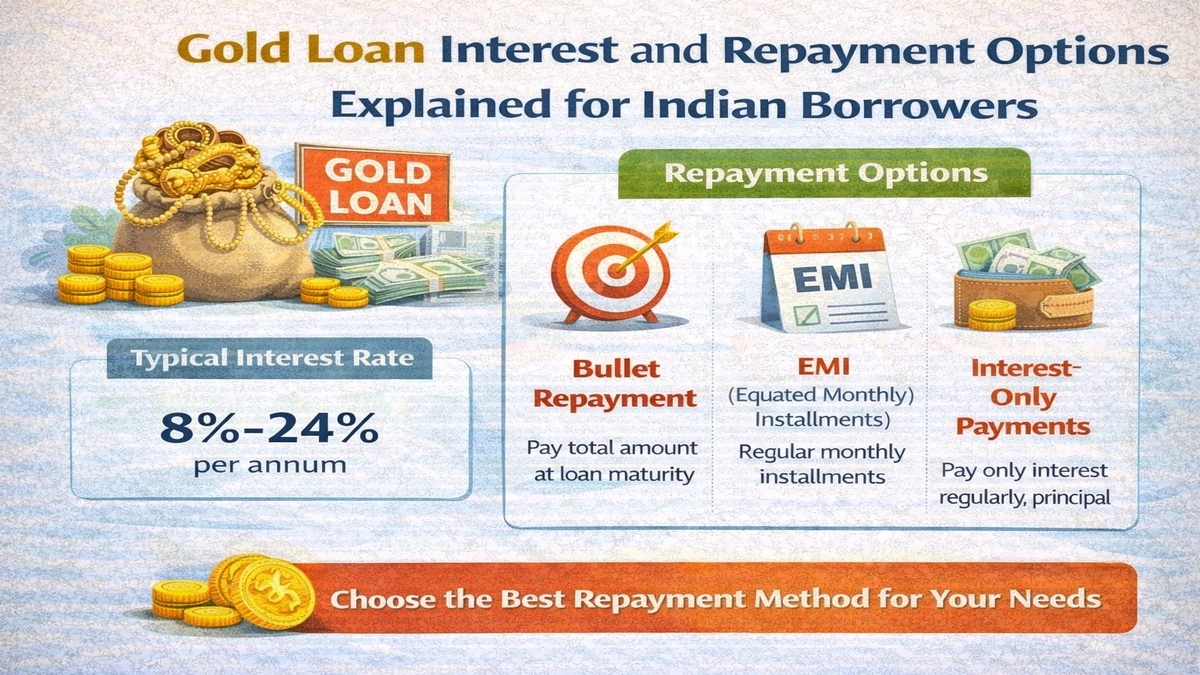

Decoding Your Options | The Main Gold Loan Repayment Schemes

When it comes to gold loans in India, you’re generally not stuck with a single, rigid repayment model. Lenders, understanding the diverse financial situations of their customers, have crafted several schemes. Knowing these is your first step towards mastering your loan. Let’s break them down:

1. The Standard EMI Option | Your Familiar Friend

This is probably the most common and recognizable repayment method, much like your home or car loan. With the EMI option, you pay a fixed amount every month. This amount includes both a portion of your principal loan amount and the gold loan interest rates. It’s predictable, it’s structured, and it’s excellent for those with a steady, regular income.

- How it works: You get a clear schedule. Each month, on a specific date, a fixed sum is debited from your account.

- Who it’s for: Salaried individuals, small business owners with consistent monthly earnings, or anyone who prefers budgeting with fixed outflows.

- Pros: Predictability, disciplined repayment, gradual reduction of principal.

- Cons: Can feel heavy if your income fluctuates.

2. The Bullet Repayment Scheme | The One-Shot Wonder

Now, this is where gold loans get a bit unique and offer incredible financial flexibility for certain borrowers. The bullet repayment scheme is exactly what it sounds like: you pay the entire principal amount and the accumulated interest in one go, at the end of the loan tenure. During the loan period, you only pay the interest, often monthly or quarterly, or sometimes, even nothing until maturity!

- How it works: You borrow, use the funds, and only settle the full principal and accumulated interest at the very end.

- Who it’s for: Farmers waiting for harvest season, traders expecting a large payment, or anyone with a clear, short-term need for funds who anticipates a lump sum income in the near future. It’s typically offered for shorter loan tenures, often up to 6 or 12 months.

- Pros: Low immediate financial burden, great for short-term cash flow gaps.

- Cons: Requires significant discipline to save the lump sum, high risk if the anticipated income doesn’t materialize.

3. The Interest-Only Repayment | A Hybrid Approach

This scheme is a bit of a middle ground. Here, you pay only the interest amount on a monthly, quarterly, or semi-annual basis. The principal amount remains untouched until the end of the loan tenure, at which point you repay the full principal. It’s distinct from bullet repayment because you are making regular interest payments, preventing the interest from compounding as aggressively.

- How it works: Regular interest payments keep your account active, but the principal is a balloon payment at the end.

- Who it’s for: Individuals who want to keep their monthly outgoings low but have a clear plan to repay the principal in one go later. It’s often preferred for slightly longer tenures than bullet schemes.

- Pros: Reduced monthly burden compared to EMI, better interest management than bullet repayment.

- Cons: Still requires a large principal payment at the end.

Making the Smart Choice | Factors to Consider for Your Repayment Plan

Choosing the right repayment schemes isn’t about picking the ‘best’ one in isolation; it’s about picking the best one for you. Think of it as tailoring a suit – one size definitely doesn’t fit all. Here’s how I advise people to think through it:

1. Your Income Flow | Steady or Seasonal?

This is paramount. If you’re a salaried professional with a predictable paycheck, the gold loan EMI options make perfect sense. You know what’s coming in, so you can plan what’s going out. But if you’re a farmer, a small business owner with seasonal revenue, or someone expecting a bonus or maturity payout, a bullet repayment or interest-only plan might offer the flexibility you desperately need. Don’t force a square peg into a round hole.

2. The Loan Tenure | Short Term vs. Long Haul

Most gold loans are short-to-medium term, typically ranging from 3 months to 3 years. Bullet repayment is almost exclusively for shorter tenures (often under a year). If you need a longer repayment period, EMI or interest-only options will be more prevalent. The longer the loan tenure, the more important it is to have a sustainable monthly payment plan.

3. Your Discipline and Financial Habits

Let’s be brutally honest with ourselves here. If you struggle with saving and tend to spend any extra cash, the bullet repayment option could be a trap. The temptation to not save for that final lump sum can be immense. For such individuals, the forced discipline of an EMI is a blessing in disguise. If you’re a meticulous planner and saver, then the flexibility of bullet repayment could be a significant advantage.

4. The Interest Rate | A Closer Look

While the repayment structure is vital, don’t forget the interest rates themselves. Different schemes might come with slightly varying rates, or the effective cost might differ based on how interest is calculated. Always ask for the Annual Percentage Rate (APR) to compare apples to apples. A slightly higher rate on a flexible plan might still be worth it if it prevents financial strain.

Beyond the Basics | Early Closure, Partial Payments, and What Ifs

Life is unpredictable, and your loan management should be agile enough to handle it. So, what happens if you suddenly come into some funds or want to reduce your burden?

Can I do a Partial Gold Loan Repayment?

Absolutely, and this is a fantastic feature of many gold loans. Most lenders allow for partial gold loan repayment. This means you can pay off a portion of your principal loan amount before the due date. The benefit? Your outstanding principal reduces, which in turn reduces the interest you’ll pay over the remaining loan tenure. It’s a smart way to manage your debt and reduce your overall cost. Always check with your lender about their specific terms for partial payments – some might have minimum amounts or specific windows.

How to Close Gold Loan Early?

This is often the dream scenario, right? You want to be debt-free. Most gold loans allow for early closure without significant penalties, unlike many other loan types. You simply pay the outstanding principal plus any accumulated interest up to the date of closure. I’ve often seen people use unexpected bonuses or windfalls to do this, and it’s always a commendable financial move. Just ensure you get a ‘No Due Certificate’ from your lender once the loan is fully settled.

What if I Miss a Payment?

Missing a payment, whether it’s an EMI or an interest installment for a bullet loan, can lead to penalties and a higher effective interest rate. It’s crucial to communicate with your lender immediately if you foresee a problem. They might offer solutions or grace periods. Ignoring it is the worst possible approach, as it can escalate into higher charges and even impact your credit score, making futurefinancial planningmore challenging.

Pro Tips for a Smooth Journey | Expert Advice on Managing Your Gold Loan

Having guided many through their financial decisions, I’ve picked up a few invaluable tips that make a world of difference:

- Read the Fine Print, Seriously: Before signing anything, understand all the terms and conditions, especially regarding interest calculation, late payment fees, and prepayment clauses. Don’t just skim it.

- Set Reminders: Whether it’s for an EMI or a bullet payment deadline, set multiple reminders. A simple calendar alert can save you from late fees and stress.

- Regularly Check Your Balance: Keep tabs on your outstanding principal and interest. Many lenders offer online portals or apps for a quick gold loan balance check. This helps you stay informed and plan for partial payments or early closure.

- Don’t Over-Leverage: While gold loans offer significant value, don’t borrow more than you absolutely need or can comfortably repay. Just because you can get a higher amount doesn’t mean you should.

- Consider Refinancing: If interest rates drop significantly, or your financial situation changes, explore the option of refinancing your gold loan with another lender offering better terms. It’s a competitive market!

For more detailed information on specific lender policies or current regulations, it’s always a good idea to consult official banking sites or financial news portals. For instance, you can often find general financial guidance on platforms likeInvestopedia.

FAQs About Gold Loan Repayment

What is the most flexible gold loan repayment option?

Generally, the Bullet Repayment Scheme offers the most flexibility as it allows you to pay the entire principal and accumulated interest at the end of the loan tenure, with little to no payments during the interim period. However, it requires strong financial discipline.

Can I change my gold loan repayment option mid-tenure?

It depends on the lender’s policy. Some lenders might allow you to switch between EMI and interest-only options, or vice-versa, with certain conditions or fees. It’s best to discuss this with your bank or NBFC directly.

Are there any hidden charges for early closure of a gold loan?

Most gold loans in India do not levy prepayment penalties, especially if they are for personal use. However, always confirm this with your specific lender before taking the loan, as policies can vary. Transparency is key here.

How do gold loan interest rates compare across different repayment schemes?

While the base interest rate might be similar, the effective cost can vary. Bullet repayment schemes, due to their higher risk for the lender, sometimes have slightly higher interest rates or specific conditions. Always compare the Annual Percentage Rate (APR) for the specific scheme you’re considering.

What happens if I can’t repay my gold loan?

If you fail to repay your gold loan, the lender will first send reminders and notices. If repayment is still not made, after a specified period (as per your loan agreement and regulatory guidelines), the lender has the right to auction your gold collateral to recover their dues. This is why understanding your gold loan repayment options explained is so vital.

So, there you have it. Choosing a gold loan repayment plan isn’t a throwaway decision; it’s a strategic one that can profoundly impact your financial well-being. By understanding the different schemes, assessing your own financial situation, and being proactive, you can ensure your gold loan serves its purpose without adding any unnecessary burdens. Remember, knowledge is power, especially when it comes to your money!