Alright, let’s be honest for a moment. That initial excitement of driving a new (or new-to-you) car often comes with a bit of a sting: the monthly payment. Maybe your credit wasn’t stellar back then, or perhaps interest rates have shifted dramatically. Whatever the reason, if you’re reading this, you’re likely wondering, “Is there a way out of this monthly grind? Can I really get a better deal?” The answer, my friend, is a resounding yes, and it’s called auto loan refinancing. But here’s the thing: it’s not just about finding a lower rate; it’s about understanding the ‘how’ so you can truly optimize your financial situation. I’ve seen countless people jump into this without a clear strategy, only to find marginal improvements. Let me guide you through the process, step-by-step, ensuring you make the most informed decisions.

This isn’t just about saving a few bucks; it’s about reclaiming control over your budget and freeing up cash for other important things, whether it’s building an emergency fund, tackling other debts, or finally taking that road trip. So, grab a coffee, and let’s demystify how to refinance car loan USA.

The “Why Now?” — Understanding Your Refinancing Triggers

Before we dive into the nitty-gritty of the process, it’s crucial to understand why you’re even considering this. Refinancing isn’t a one-size-fits-all solution, but several common scenarios make it a brilliant move:

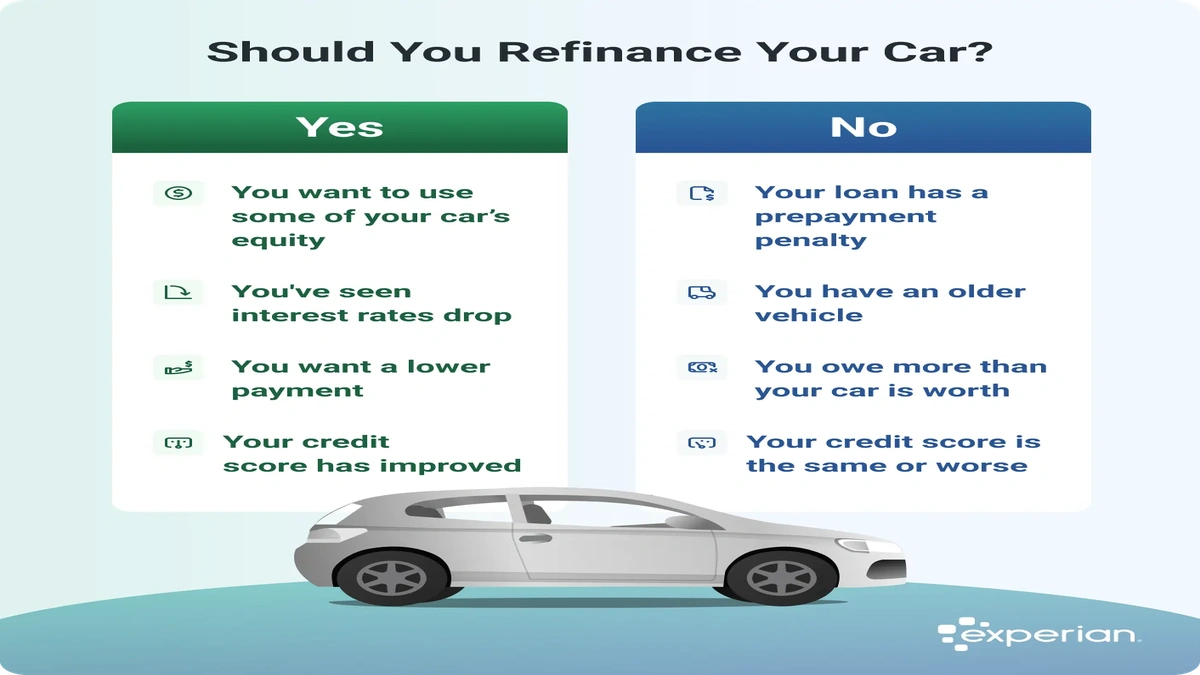

- Your Credit Score Has Improved: This is perhaps the most common and impactful reason. If your credit score has climbed significantly since you first took out the loan, you’re now seen as a less risky borrower. This means you qualify for better car loan interest rates. It’s like getting a gold star for being responsible!

- Interest Rates Have Dropped: The market fluctuates. If general interest rates have fallen since your original purchase, you might be able to secure a significantly lower rate, even if your credit hasn’t changed.

- You Want to Lower Your Monthly Payments: This often goes hand-in-hand with a lower interest rate, but sometimes it also involves extending the loan terms. Be careful here – while lower payments sound great, a longer term means you’ll pay more interest overall. It’s a trade-off to consider based on your immediate cash flow needs.

- You Want to Shorten Your Loan Term: Conversely, if your financial situation has improved, you might want to pay off the car faster, saving a substantial amount on interest. This usually means a higher monthly car payments but a quicker path to ownership.

- You Need to Remove a Co-signer: Sometimes, a co-signer was necessary to get the original loan. If your credit is now strong enough, refinancing allows you to remove them, freeing them from the obligation.

- Debt Consolidation: While less common for car loans, some people use refinancing to simplify their finances, especially if they have high-interest personal loans. However, remember that a car loan is secured debt, meaning your car can be repossessed if you default.

Understanding your primary motivation will help you evaluate the refinance options and choose the best path forward. It’s not just about seeking the lowest rate, but the right rate and terms for your goals.

The Nitty-Gritty | Your Step-by-Step Guide to Refinancing

Okay, let’s get practical. Here’s how you actually go about refinance your car loan without feeling overwhelmed.

Step 1 | Gather Your Documents and Know Your Numbers

Before you even think about approaching new lenders, you need to know exactly where you stand. This means:

- Current Loan Information: Dig out your original loan agreement. You’ll need your current interest rate, remaining balance, and payoff amount. Your current lender can provide an official payoff quote.

- Vehicle Information: Make, model, year, VIN (Vehicle Identification Number), and current mileage.

- Personal Financials: Proof of income (pay stubs, tax returns), employment history, and a good understanding of your credit score impact. Many online services offer free credit score checks, which is a great starting point. Remember, lenders will pull their own, but knowing yours gives you an advantage.

A quick mental check: Is your car worth less than you owe on it (upside down)? If so, refinancing can be trickier, but not impossible. Some lenders offer specific programs, though the rates might not be as attractive. This is also where anauto loan pre-approval online USAcan be a real game-changer, giving you a clear picture of what you qualify for before committing.

Step 2 | Shop Around, Shop Around, Shop Around!

This is arguably the most critical step. Do NOT just go with the first offer you get. Different lenders (banks, credit unions, online lenders) have different criteria and offer varying rates. What fascinates me is how much rates can differ even for someone with an excellent credit score. Use an auto loan refinance calculator online to get a ballpark idea of what different rates and terms would mean for your lower car payments.

When comparing offers, look beyond just the interest rate:

- APR (Annual Percentage Rate): This includes the interest rate plus any fees, giving you the true cost of the loan.

- Loan Term: How long will you be paying? A shorter term means more savings on interest.

- Fees: Are there any origination fees, application fees, or prepayment penalties?

Remember, applying with multiple lenders within a short window (typically 14-45 days, depending on the credit scoring model) counts as a single inquiry on your credit report, so don’t be afraid to compare widely. This is your money we’re talking about!

Step 3 | Submit Your Application and Finalize the Deal

Once you’ve found the best offer, it’s time to formally apply. This will involve providing all the documents you gathered in Step 1. The lender will review everything, verify your information, and then give you a final offer. Read the fine print! Seriously, every single line. Ensure the terms match what you were promised and that there are no hidden surprises.

Once approved, the new lender will pay off your old loan, and you’ll start making payments to them. It’s surprisingly seamless, but the due diligence on your part is what makes it truly beneficial.

Navigating the Tricky Bits | When Refinancing Gets Complicated

While the process sounds straightforward, life often throws curveballs. Here are a few common scenarios and how to approach them:

What if I have Bad Credit?

This is a common concern. While a stellar credit score gets you the best rates, having bad credit car refinance options still exist. Look for lenders specializing in subprime loans, or consider adding a co-signer with good credit to your application. You might not get the absolute lowest rate, but even a slight improvement can lead to meaningful savings over the life of the loan. Focus on demonstrating a stable income and a consistent payment history since your original loan.

When is the Best Time to Refinance a Car?

The best time to refinance car loan is typically when your credit score has improved, market interest rates have dropped, or your current loan has a high interest rate. It’s also smart to consider if you’re approaching the mid-point of your loan term; refinancing too late might not save you as much in interest, as you’ve already paid a significant portion of the interest upfront in the earlier years of the loan (due to amortization schedules).

However, if you’re looking for flexibility in your financial situation or exploring ways to manage your business’s capital, understanding options like acollateral free business loan Indiacan also provide valuable insights into managing debt strategically, even if it’s a different context.

FAQs | Your Quick Questions Answered

Frequently Asked Questions About Car Loan Refinancing

Can I refinance my car loan with the same lender?

Yes, you can. However, it’s generally advisable to shop around with multiple lenders, including your current one. Your existing lender might offer you a better deal to retain your business, but you won’t know if you’re getting the best possible rate unless you compare it with others.

How long does it take to refinance a car loan?

The entire process, from application to approval and payoff, can take anywhere from a few days to a couple of weeks. Online lenders often have quicker turnaround times than traditional banks or credit unions.

What credit score do I need to refinance a car loan?

While there’s no hard and fast rule, a FICO score of 660 or higher is generally considered good enough to qualify for competitive rates. Scores above 700 will likely get you the best offers. However, even with scores in the 500s or 600s, you might still find refinance options, though the interest rates will be higher.

Will refinancing hurt my credit score?

Initially, yes, slightly. Lenders will perform a hard inquiry on your credit report, which can temporarily drop your score by a few points. However, if you secure a lower interest rate and consistently make on-time payments, the long-term positive impact on your credit score and overall financial health will far outweigh the initial dip.

What if my car is too old or has too many miles?

Most lenders have restrictions on the age and mileage of vehicles they will refinance. Typically, cars older than 7-10 years or with more than 100,000-120,000 miles can be difficult to refinance. However, some specialized lenders might still offer refinance options, albeit with potentially higher rates.

The Final Word | Take Control of Your Car Loan

Refinancing your car loan isn’t just about shuffling paperwork; it’s a powerful financial tool that, when used correctly, can significantly improve your cash flow and reduce your overall debt burden. It’s an act of financial empowerment. By following these steps and understanding the nuances, you’re not just saving money; you’re becoming a smarter, more strategic consumer. Don’t let your car payment dictate your budget – take charge, explore your options, and drive towards a more financially comfortable future. Happy refinancing!