Let’s be honest, the phrase “student loans” can feel like a heavy weight, right? For millions across the student loans USA landscape, it’s not just a financial burden; it’s a constant, nagging presence. We’re talking about a colossal sum, often stretching into six figures, that can dictate life choices, delay dreams, and frankly, keep you up at night. You’ve probably heard the horror stories, or maybe you’re living one yourself – the seemingly endless monthly payments that barely touch the principal, the escalating interest, the feeling of being trapped. But what if I told you there’s a crucial, often misunderstood, mechanism designed to ease that burden significantly? I’m talking about income driven repayment plans, and understanding why they exist and how they work is more vital now than ever before.

This isn’t just about tweaking a few numbers; it’s about a fundamental shift in how we approach student loan debt in America. It’s about ensuring that a college degree, while an investment, doesn’t become a lifelong financial prison. As an analyst, what truly fascinates me about IDR isn’t just the lower payments, but the profound impact it can have on a borrower’s overall financial future, providing a much-needed safety net. Let’s peel back the layers and understand why IDR isn’t just a “nice-to-have” option, but a potential game-changer for your peace of mind and your wallet.

The Looming Shadow of Student Debt | Why IDR Isn’t Just a “Nice-to-Have”

The numbers are staggering. Over 43 million Americans carry federal student loans, collectively owing trillions. For many, the idea of a standard 10-year repayment plan is simply untenable. Imagine graduating with a degree, eager to start your career, only to be hit with a loan payment that rivals your rent. It’s a setup that often forces people into difficult choices: delay starting a family, postpone buying a home, or even put off essential healthcare. This isn’t just a personal problem; it’s an economic one, stifling growth and innovation.

The traditional repayment model, while straightforward, often fails to account for the realities of early career earnings, economic downturns, or unexpected life events. It assumes a steady, predictable income trajectory that simply isn’t a given for everyone. This is precisely why income driven repayment plans were conceived: to create a more equitable system. They acknowledge that your ability to pay should be directly linked to your current income, not just the original loan amount. It’s a safety valve, designed to prevent default and, more importantly, to allow you to live your life while responsibly addressing your debt. Without IDR, the entire system would buckle under the weight of defaults, impacting not just borrowers but the broader economy. It’s an essential piece of the puzzle, a foundational element for managing the massive scale of student loan debt in the country.

Decoding IDR | More Than Just Lower Payments (The Hidden Mechanics)

So, what exactly is income driven repayment? At its core, it’s a suite of federal student loan repayment options that adjust your monthly payments based on your income and family size. Instead of a fixed amount, your payment becomes a percentage of your discretionary income. This means if your income is low, your payments could be significantly reduced, sometimes even to zero. This flexibility is its superpower.

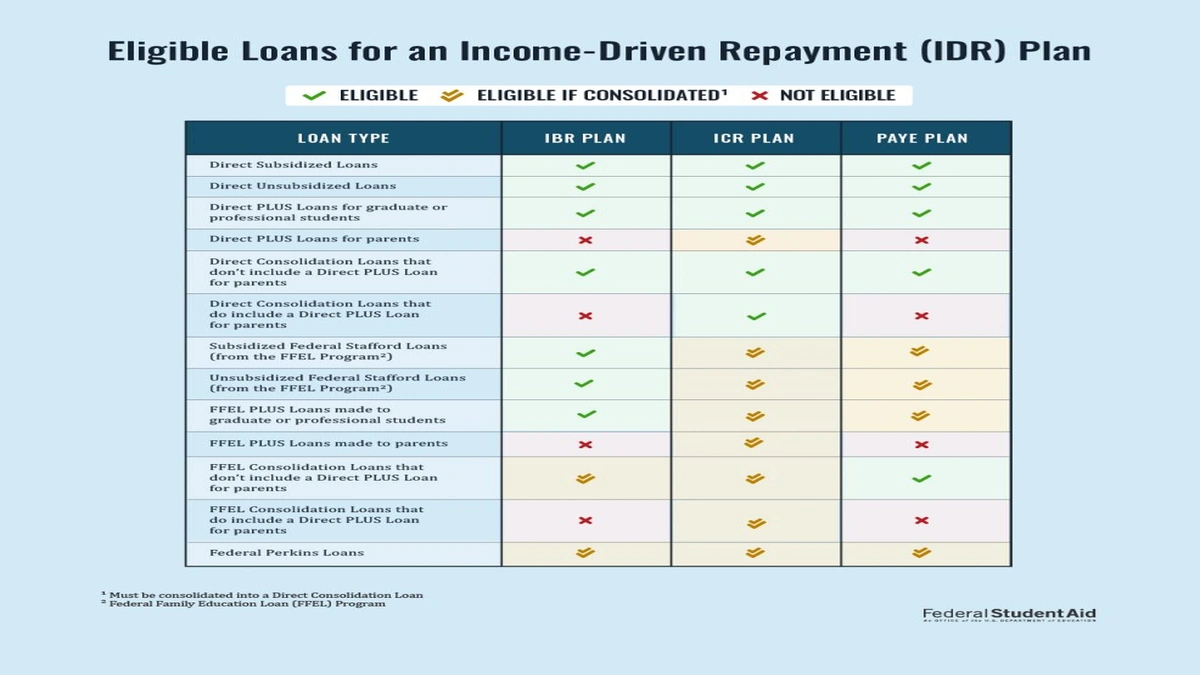

Historically, there have been several IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR). But let me tell you, the real buzz right now is around the new SAVE Plan student loans (Saving on a Valuable Education). This plan, which replaced the REPAYE plan, is a game-changer. Why is it such a big deal? Well, for starters, it significantly reduces how your discretionary income is calculated, meaning lower payments for many. Even better, it includes an interest subsidy, preventing your loan balance from growing due to unpaid interest if your payment doesn’t cover it. This is a massive relief for those who’ve watched their loan balances balloon despite making regular payments.

Understanding these nuances is crucial because selecting the right plan can save you thousands. Each plan has slightly different eligibility requirements and payment calculation methods. And here’s where your loan servicers come in. They are the companies that manage your loans, and they can help you navigate these options. However, it’s vital to be proactive and informed yourself, as not all servicers are equally adept at explaining every intricate detail. You might even find yourself comparing their service levels, much like you’d compare options for agold loan interest rate comparison 2026to ensure you’re getting the best terms and support.

Navigating the Maze | How to Find Your Best Federal Student Loan Repayment Options

Alright, so you’re convinced IDR might be for you. Now what? The process, while not overly complicated, requires attention to detail. First, you need to determine which federal student loan repayment options you qualify for. Not all loans are eligible for every IDR plan, though most direct federal loans are.

Your starting point should always be StudentAid.gov. This is the official hub for all things federal student loans. They have an excellent income driven repayment calculator that allows you to input your income, family size, and loan amounts to get an estimate of your monthly payments under different IDR plans, including the SAVE Plan. I can’t stress this enough: use that calculator! It provides invaluable foresight.

To apply, you’ll typically need to provide documentation of your income (like tax returns or pay stubs) and family size. The application can usually be completed online through your loan servicers’ portal or directly on StudentAid.gov. A common mistake I see people make is forgetting about annual recertification. Why is this so critical? Because your income and family size can change! If you don’t recertify annually, your payments could revert to the standard plan, leading to a nasty surprise. It’s like forgetting to renew your gym membership and suddenly being charged a much higher drop-in rate – a preventable headache.

Being organized with your financial documents, much like keeping track of yourhome loan processing fees comparison, can save you a lot of stress down the line. Keep copies of everything you submit, and make a note of when your recertification is due.

The Golden Ticket | Understanding Student Loan Forgiveness Through IDR

Here’s the part that truly excites many borrowers: the prospect of student loan forgiveness. All income driven repayment plans offer forgiveness of any remaining loan balance after a certain number of years – typically 20 or 25 years of qualifying payments. This means that if you consistently make your reduced payments under an IDR plan for the specified period, the rest of your student loan debt can be wiped clean. Why is this so important? Because it provides a light at the end of the tunnel, a definitive end date to your repayment journey, even if your payments are low.

For those working in public service, there’s an even faster track: Public Service Loan Forgiveness (PSLF). This program allows for forgiveness after just 10 years (120 qualifying payments) if you work for a qualifying non-profit organization or government agency. It’s a powerful incentive that acknowledges the value of public service. The key here is that you must be on a qualifying IDR plan and working for a qualifying employer. PSLF has had its complexities in the past, but recent reforms have made it more accessible and reliable, which is a huge win for those dedicating their careers to helping others.

It’s important to note that historically, forgiven balances under IDR (outside of PSLF) could be considered taxable income by the IRS. However, current legislation has temporarily waived this tax until 2025, a significant relief for many. Always stay updated on the latest tax laws or consult a tax professional. For more details on the intricacies of federal student loan programs and loan forgiveness, the officialStudentAid.govwebsite is your definitive source.

Beyond the Numbers | The Real Impact on Your Financial Future

While the numbers are compelling, the true value of income driven repayment extends far beyond mere calculations. It’s about giving you breathing room. When your monthly payments are manageable, you’re not just avoiding default; you’re able to invest in other areas of your life. This could mean saving for a down payment on a house, starting a family, pursuing further education without adding crushing debt, or simply building an emergency fund. Why does this matter? Because financial stability is foundational to overall well-being.

Consider the psychological benefit. The stress of overwhelming student loan debt can be debilitating. Knowing that your payments are tied to your income, and that there’s a path to loan forgiveness, can alleviate a significant amount of anxiety. It allows you to focus on career growth, knowing that a temporary dip in income won’t derail your entire financial future. Furthermore, in an environment where student loan interest rates can feel punitive, IDR plans, especially the SAVE Plan, offer protection against runaway interest accumulation, ensuring your balance doesn’t become an insurmountable mountain.

Ultimately, IDR plans represent a commitment to accessibility and sustainability within higher education. They acknowledge that the journey after graduation can be unpredictable and provide a flexible framework to navigate it. It’s not a magic bullet, but it is a powerful tool in your financial arsenal, ensuring that your education remains an asset, not an albatross.

Frequently Asked Questions About Income-Driven Repayment

What is the difference between the SAVE Plan and other IDR plans?

The SAVE Plan student loans (Saving on a Valuable Education) generally offers the lowest monthly payments among IDR plans because it calculates discretionary income more favorably (225% of the poverty line, up from 150%) and provides an interest subsidy to prevent your balance from growing if your payment doesn’t cover the full interest.

Who is eligible for income-driven repayment plans?

Most federal student loans are eligible for at least one IDR plan. This includes Direct Subsidized and Unsubsidized Loans, Direct PLUS Loans made to students, and Direct Consolidation Loans. FFEL Program loans may also become eligible after consolidation into a Direct Consolidation Loan.

How do I apply for or renew my IDR plan?

You can apply or renew your IDR plan online at StudentAid.gov or through your loan servicer. You’ll need to provide information about your income and family size. Remember to recertify annually to keep your payments adjusted to your current financial situation.

Can my monthly payment be $0 under an IDR plan?

Yes, absolutely! If your income is low enough relative to your family size and the federal poverty guidelines, your calculated monthly payments under an IDR plan can indeed be $0. These $0 payments still count towards your required payment period for loan forgiveness.

What happens if I miss my annual IDR recertification deadline?

If you miss your annual recertification, your loan servicers will likely place you on the standard repayment plan, and your monthly payments could increase significantly. Any unpaid interest might also capitalize (be added to your principal balance), increasing your total debt. It’s crucial to stay on top of your deadlines.

Does private student loan debt qualify for income-driven repayment?

No, income driven repayment plans are exclusively for federal student loans. Private student loan debt does not qualify for IDR or federal loan forgiveness programs like PSLF. Private lenders may offer their own hardship options, but they are not standardized federal programs.