Alright, let’s be honest. When you hear ” mortgage refinance rates UK today ,” your eyes might glaze over a little. It sounds like something only a finance wizard or someone with far too much time on their hands would obsess over, right? But here’s the thing: for hundreds of thousands of homeowners across the UK, what’s happening with these rates right now isn’t just a headline it’s a massive, wallet-shaking reality. And frankly, understanding the ‘why’ behind these shifts could be one of the smartest financial moves you make all year.

I’ve seen firsthand how easily people can get caught off guard. One minute you’re happily paying your monthly mortgage, the next you’re staring at an email from your lender, or worse, a news report, and panic starts to creep in. That pit-of-the-stomach feeling? Totally understandable. But what if I told you that by understanding the deeper currents at play, you could turn that anxiety into a strategic advantage?

This isn’t just about quoting numbers; it’s about understanding the pulse of the UK remortgage market and what it truly means for your home, your finances, and your peace of mind. Let’s dive in, shall we?

The Shifting Sands | Why UK Mortgage Refinance Rates Are Never Static

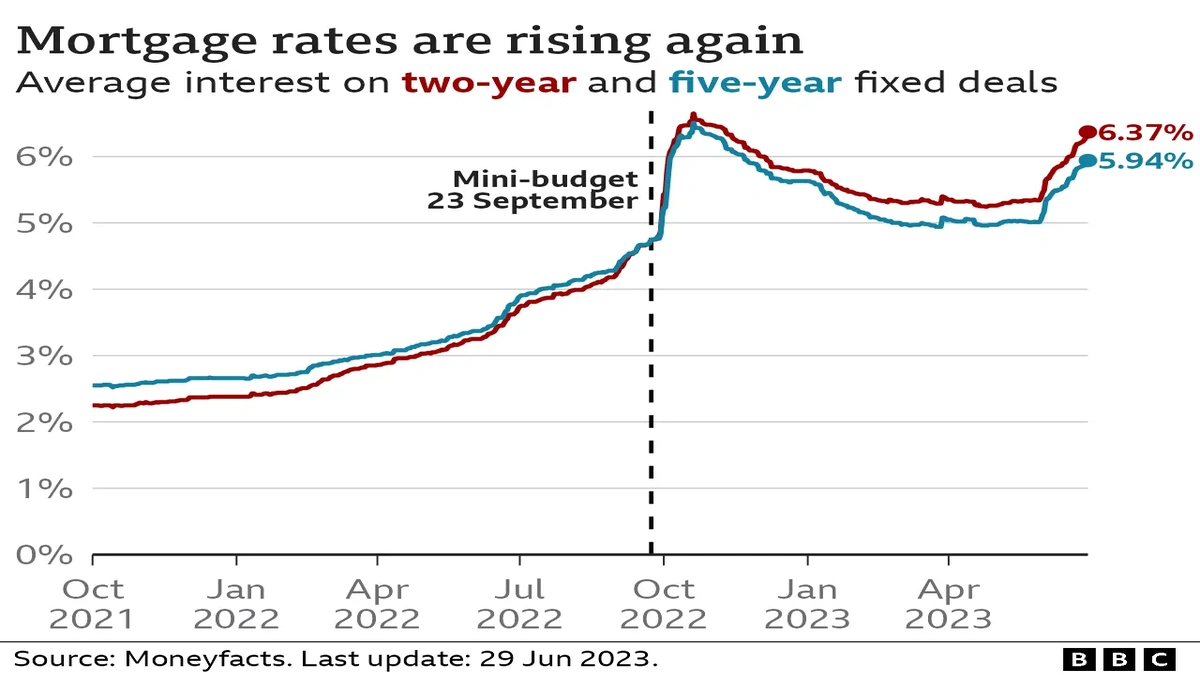

Think of the financial world as a giant, intricate clockwork mechanism. At its heart, especially for us homeowners in the UK, is the Bank of England’s base rate. This isn’t just a number; it’s the fundamental cost of money for banks, and it dictates, to a large extent, what they charge you for your mortgage. So, when we talk about what’s influencing mortgage refinance rates UK today , we’re really talking about what’s influencing the Old Lady of Threadneedle Street.

What fascinates me is how many factors feed into this. Inflation, for instance, is a massive driver. If the cost of living is soaring, the Bank of England often steps in to cool the economy down by raising interest rates. The idea is to make borrowing more expensive, encouraging people to save rather than spend, which theoretically brings prices back under control. But it’s a delicate balancing act, isn’t it?

Then there’s the broader economic outlook. Are we seeing growth or recession? What’s happening in global markets? Even geopolitical events can send ripples through bond markets, which in turn affect the long-term funding costs for lenders. This complex interplay means that the Bank of England base rate , and consequently your mortgage rates, are always in flux. It’s like trying to predict the British weather – you can have a good guess, but there are always surprises!

TheBank of England’s Monetary Policy Committeemeets regularly to assess these factors, and their decisions are the big news that often sends shivers or sighs of relief through the UK remortgage market . Understanding their rationale, as outlined in their official reports, gives you a significant edge in anticipating future movements.

Fixed vs. Variable | Decoding Your Options in Today’s Market

So, you’re looking at your current deal expiring, or perhaps you’re just fed up with the rate you’re on. The big question looms: should you go for a fixed-rate mortgages or brave the world of variable rates ? This is where the rubber meets the road, and your personal risk tolerance really comes into play. It’s not a one-size-fits-all answer, and a common mistake I see people make is simply picking what their friend chose without truly understanding their own situation.

Fixed-rate mortgage deals offer stability. You lock in an interest rate for a set period say, two, five, or even ten years and your monthly payments remain predictable, come what may. In times of uncertainty, or when interest rates are expected to rise, this offers immense peace of mind. You know exactly what you’re paying, allowing for easier budgeting. However, if rates unexpectedly drop significantly, you might find yourself stuck on a higher rate, potentially missing out on cheaper deals.

On the other hand, variable mortgage rates , like tracker mortgages or standard variable rates (SVRs), fluctuate with the Bank of England base rate. When the base rate goes up, your payments go up. When it comes down, your payments go down. This can be fantastic in a falling rate environment, but it carries inherent risk. Your payments could suddenly jump, putting a strain on your finances. It’s a gamble, albeit one that can pay off if you’re confident in your ability to absorb potential increases or if you believe rates are on a downward trend.

Calculating the potential impact of different rates is crucial. Tools like ahome loan EMI calculatorcan be incredibly helpful here, letting you model various scenarios and see how changes in interest rates or loan terms affect your monthly outgoings. It’s about taking control, not just hoping for the best.

Beyond the Headline Rates | Hidden Costs and Considerations

When you’re poring over those tempting new remortgage deals , it’s easy to get fixated on the interest rate alone. But trust me, as someone who’s delved deep into these things, the rate is just one piece of a much larger, and sometimes pricier, puzzle. What often gets overlooked are the ‘hidden’ costs – the fees that can quietly eat into any potential savings.

First up, early repayment charges . If you’re remortgaging before your current fixed or tracker deal expires, your existing lender will almost certainly hit you with a penalty. This can be a significant sum, often a percentage of the outstanding loan, and it’s absolutely vital to factor this into your calculations. Sometimes, the cost of breaking free outweighs the benefit of a slightly lower rate elsewhere.

Then there are the arrangement fees, also known as product fees. These can range from a few hundred to several thousand pounds, depending on the deal. Some lenders offer fee-free mortgages, but often with a slightly higher interest rate. You have to weigh up whether paying the fee upfront for a lower rate makes sense for your specific situation and how long you plan to stay on that deal. Legal fees and valuation fees are also part of the package, even if your new lender offers a ‘free’ valuation, there are still legal costs involved in transferring the mortgage. It’s a lot to keep track of, isn’t it?

This is where professional advice becomes invaluable. Engaging with a reputablemortgage broker advicecan save you money and headaches. They have access to a wider range of deals, can help navigate the complexities, and ensure you’re not caught out by unexpected charges. They’ll also assess your mortgage affordability rigorously, a crucial step in today’s lending environment.

Navigating the Remortgage Journey | A Step-by-Step Insight

Alright, so you’ve done your homework, understood the ‘why’ and the ‘how’ of the rates, and now you’re ready to actually remortgage. What does that journey look like? It’s not as daunting as it might seem, especially if you break it down. And believe me, having a clear roadmap can make all the difference, much like planning your business’sworking capital guide; preparation is key to success.

First, timing is everything. Start looking for new deals about three to six months before your current one expires. This gives you ample time to compare, apply, and get everything processed without rushing. Many lenders will offer you a rate that you can ‘reserve’ for a period, giving you flexibility.

Next, gather your documents. This usually includes proof of income (payslips, tax returns), bank statements, utility bills, and details of your existing mortgage. Lenders will also perform a credit check and assess your affordability criteria UK . Be prepared for them to scrutinize your spending habits and income, as they need to ensure you can comfortably meet the repayments, especially if interest rate predictions suggest potential increases.

Once you’ve chosen a deal and applied, the process involves a valuation of your property (to ensure the loan-to-value or LTV is acceptable), legal work to switch the charge from your old lender to the new one, and finally, completion. It’s a structured process, but it requires diligence on your part to provide information promptly and chase up any delays. Think of it as a financial marathon, not a sprint.

What Lies Ahead? Interest Rate Predictions and Your Next Move

If only we had a crystal ball, right? Predicting the exact trajectory of mortgage refinance rates UK today is impossible. However, we can look at expert forecasts and market sentiment to make educated guesses. The general consensus from economists and financial institutions often points to a continuation of the Bank of England’s strategy to manage inflation, which means rate movements will largely hinge on economic data.

What does this mean for you? It means staying informed is paramount. Don’t just rely on headline news. Follow reputable financial commentators, read the analysis from major banks, and keep an eye on official announcements from the Bank of England. Remember, these are predictions, not guarantees, and the market can always throw a curveball. The key is to be agile and prepared for different scenarios.

Ultimately, your ‘next move’ should be a proactive one. Don’t wait until your current deal is about to expire to start thinking about it. Regularly review your mortgage, perhaps once a year, even if you’re locked into a long-term fixed rate. Conditions change, your personal circumstances change, and what was the best deal for you five years ago might not be the best now.

Frequently Asked Questions About UK Mortgage Refinance Rates

What exactly is remortgaging?

Remortgaging is essentially switching your mortgage from one lender to another, or moving to a new deal with your existing lender. People do it for various reasons, like getting a better interest rate, releasing equity from their home, or consolidating debt.

How often should I check mortgage refinance rates?

It’s a good idea to start checking mortgage refinance rates UK today around six months before your current deal is due to end. This gives you plenty of time to research, compare options, and secure a new deal without rushing. Even if your deal isn’t ending soon, a quick check once a year keeps you informed.

Will my credit score affect my ability to remortgage?

Absolutely. Lenders will perform a credit check as part of your application. A strong credit score demonstrates you’re a reliable borrower, increasing your chances of being approved for the best remortgage deals . It’s wise to check your credit report periodically and address any inaccuracies.

Can I remortgage if I have a small amount of equity?

It can be more challenging. Most lenders prefer you to have at least 10-20% equity in your home, as a higher Loan-to-Value (LTV) ratio (meaning you’ve borrowed a larger proportion of the property’s value) often leads to higher interest rates or fewer available deals. However, some specialist lenders might cater to those with lower equity.

What if I want to stay with my current lender?

That’s often called a ‘product transfer’. Your current lender will offer you new deals when your existing one expires. It can sometimes be quicker and involve fewer fees than a full remortgage, but it’s crucial to compare their offers with the wider market to ensure you’re still getting a competitive rate.

Are there any government schemes to help with remortgaging?

While there aren’t specific government schemes for remortgaging to get a better rate, broader government-backed initiatives like the Mortgage Guarantee Scheme (though primarily for first-time buyers) or support for those struggling with payments (e.g., throughMoneyHelper) can indirectly impact the market or provide assistance in difficult times.

The Bottom Line | Your Mortgage, Your Future

Navigating the world of mortgage refinance rates UK today can feel like a full-time job, but it’s a critical one. The choices you make now, informed by a deeper understanding of ‘why’ rates move and ‘how’ to approach the market, will have a tangible impact on your financial health for years to come. Don’t let inertia be your most expensive mistake. Be proactive, be informed, and take control of your mortgage it’s one of your most powerful financial levers.