Alright, let’s grab a chai and really talk about something that can either build your dreams or, well, give you a few sleepless nights: personal loans. Specifically, the age-old dilemma of secured personal loan versus unsecured personal loan. You see, it’s not just about getting money; it’s about how you get it and what that choice means for your financial future here in India. What fascinates me is how often people jump into one without truly understanding the ‘why’ behind the choice, and that’s precisely what we’re going to unravel today.

It’s easy to get caught up in the shiny advertisements promising instant cash. But as a knowledgeable friend, I’m here to tell you that the distinction between a secured personal loan and an unsecured personal loan isn’t just a technicality for lenders. Oh no, it’s a fundamental fork in your financial road, impacting everything from the interest rates you pay to your eligibility, and even your peace of mind. Let me rephrase that for clarity: understanding this comparison is perhaps one of the most crucial financial literacy lessons you’ll encounter when seeking a personal loan India.

The Core Difference | Collateral – Your Friend or Foe?

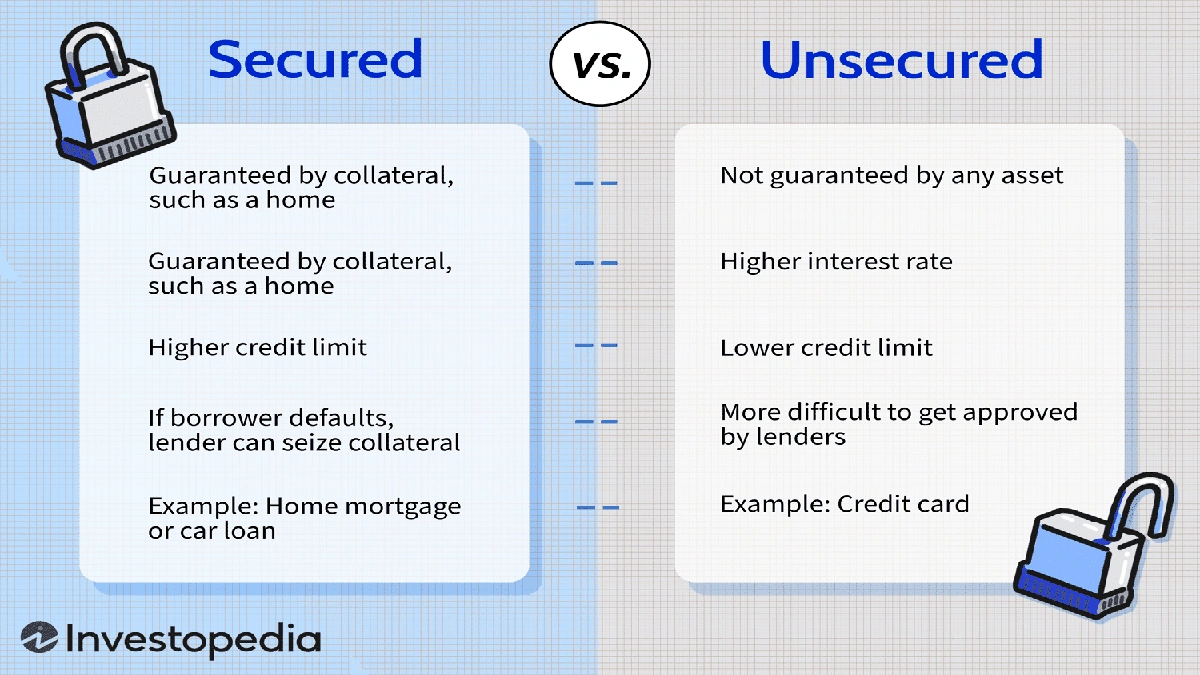

At the heart of the secured vs unsecured personal loan comparison lies one big word: collateral. Think of collateral as your promise to the bank, a valuable asset you pledge to them in case you can’t repay the loan. This could be anything from your house or car (for larger loans) to fixed deposits or gold (for specific types of collateral-backed loans). When you opt for a secured personal loan, you’re essentially putting something on the line.

Now, why does a lender care so much about this? Simple: risk. From a lender’s perspective, offering `collateral for loans` significantly reduces their risk. If you default, they can recover their money by selling the asset. This reduced risk often translates into benefits for you, the borrower. We’re talking potentially lower interest rates personal loan and sometimes, more flexible `loan repayment terms`. I initially thought this was straightforward, but then I realized the deeper implication: it gives the lender more confidence, which they pass on to you.

On the flip side, an unsecured personal loan (often called a no collateral loan) requires no such promise. You’re not pledging your beloved scooter or your ancestral jewellery. This is where your financial reputation, specifically your `credit score impact`, becomes paramount. For these loans, the lender is solely relying on your creditworthiness and your perceived ability to repay based on your income, employment history, and of course, that all-important credit score. So, for those looking for quick cash without tying up assets, `no collateral loans` might seem appealing, but they come with their own set of considerations.

A common mistake I see people make is thinking that because a loan is unsecured, it’s ‘easier.’ It might be quicker to process in some cases, but the risk assessment lender undertakes is far more stringent. They’re looking for impeccable repayment history and stable income. So, while it’s liberating not to pledge an asset, it places a heavier burden on your financial track record.

Interest Rates & Eligibility | Where the Rubber Meets the Road

This is where the ‘why’ truly hits home. When you compare secured vs unsecured personal loan, the difference in interest rates is often the most tangible factor. Generally speaking, a secured personal loan will come with lower interest rates. Why? Because of that collateral we just discussed. The lender’s risk is lower, so they can afford to charge less for the money they lend. This can save you a significant amount over the `loan repayment terms`, making your overall debt cheaper. It’s like buying insurance – you pay less if the risk is lower.

However, for an unsecured personal loan, the lender is taking a bigger gamble. To compensate for this higher risk, they typically charge higher interest rates. This is simply how the financial world balances risk and reward. So, while you might get your hands on the funds faster without any assets on the line, you’ll likely pay more for that convenience in the long run. This is crucial for personal loan eligibility India, as lenders will scrutinize your profile more intensely for no collateral loans.

Eligibility criteria also diverge. For secured personal loan options, even if your credit score isn’t stellar, having a valuable asset to pledge can sometimes open doors. It acts as a safety net. But for `unsecured personal loan` applications, your credit score is king. Lenders will look for a strong credit history, a good CIBIL score (typically 700+), and a stable income to approve your application. If you’re trying to understand more about how different financial schemes work, sometimes understanding the basics of lending can even shed light on broader financial topics likestudent loan forgiveness eligibility.

The Real-World Impact | When to Choose What

So, when should you pick which? It’s not a one-size-fits-all answer, and this is where your personal circumstances and financial goals truly matter. If you need a substantial amount, say for a major home renovation or a significant medical expense, and you have assets like a fixed deposit or gold that you’re comfortable pledging, a secured personal loan might be the more economical choice due to lower interest rates. It can also be a viable option if your credit score isn’t perfect, but you still need access to funds.

On the other hand, if you need a smaller amount for something like an unexpected expense, a quick travel plan, or even a `debt consolidation options` strategy where you want to simplify multiple high-interest debts, an unsecured personal loan can be ideal. The key here is convenience and speed, especially if you have a strong credit score and stable income. It’s about not having to go through the hassle of valuing and pledging an asset. But remember, the trade-off is often higher interest.

Consider the `loan repayment terms` too. While both types of loans offer various repayment tenures, the overall cost difference due to interest rates can make a huge impact on your monthly EMIs and the total amount repaid. It’s not just about what you can afford monthly, but what you should afford to optimize your financial stability.

Beyond the Basics | Hidden Costs and Long-Term Strategy

Beyond the obvious interest rates, there are other factors to consider in this secured vs unsecured personal loan comparison. Processing fees, pre-payment penalties, and late payment charges are common to both, but their impact can be magnified by the type of loan you choose. For instance, an unsecured loan with a higher interest rate and a pre-payment penalty might lock you into a more expensive deal for longer.

Then there’s the long-term impact on your credit score. Timely repayment of any loan, whether secured personal loan or unsecured personal loan, positively impacts your credit profile. However, defaulting on a secured personal loan not only damages your `credit score impact` but also puts your pledged asset at risk. This is a significant consideration, especially for those who might be using loans as part of a broader strategy forbusiness expansion Indiaor large personal investments.

According to financial experts at Investopedia, a secured loan provides a sense of security for the lender, which reflects in the loan terms.Understanding secured loansis fundamental to making an informed borrowing decision.

Ultimately, the choice between a secured personal loan and an unsecured personal loan isn’t about which is inherently ‘better,’ but which is ‘better for you.’ It’s about aligning the loan product with your financial capacity, your risk tolerance, and your immediate and long-term goals. Don’t just look at the `loan approval process`; look at the entire lifecycle of the loan.

Frequently Asked Questions About Personal Loans

What exactly is collateral in the context of a personal loan?

Collateral is an asset (like property, gold, or fixed deposits) that a borrower pledges to a lender as security for a loan. If the borrower defaults on the loan, the lender has the right to seize and sell this asset to recover their funds. It’s a key differentiator in the `secured vs unsecured personal loan comparison`.

Can I get an unsecured personal loan with a low credit score?

While challenging, it’s not impossible, but it will be difficult. Lenders rely heavily on your credit score for unsecured personal loan approval because there’s no collateral. A low score might lead to higher interest rates, stricter `loan repayment terms`, or outright rejection. Building a good credit history is crucial.

Are interest rates always lower for secured personal loans?

Generally, yes. Because a secured personal loan carries less risk for the lender due to the pledged collateral, they typically offer lower interest rates compared to unsecured personal loan options. However, the exact rate depends on various factors including the lender, your profile, and market conditions.

What happens if I default on a secured personal loan?

If you default on a secured personal loan, the lender has the legal right to take possession of your pledged collateral and sell it to recover the outstanding loan amount. This will also severely damage your `credit score impact` and future borrowing capacity.

Is it possible to convert an unsecured loan to a secured one?

Typically, no. Once a loan is disbursed as unsecured, it generally remains that way. However, you might be able to explore options like taking out a new secured personal loan to consolidate and pay off your existing unsecured personal loan, effectively converting the debt in a roundabout way.

Which type of personal loan offers faster approval?

While both can be quick, unsecured personal loan applications often have a faster `loan approval process` as they don’t require the time-consuming valuation and pledging of collateral. However, this is contingent on having a strong credit score and meeting all eligibility criteria swiftly.

So, there you have it. The choice between a secured personal loan and an unsecured personal loan is more than just a tick-box exercise. It’s a strategic financial decision that can shape your immediate spending power and your long-term financial stability. Take your time, weigh the pros and cons, and choose wisely. Your future self will thank you for understanding these hidden truths.