Ah, the open road! The wind in your hair, the hum of the engine, the sheer joy of zipping through traffic or cruising down a scenic highway. For many of us in India, a two-wheeler isn’t just a mode of transport; it’s a symbol of independence, a daily companion, and sometimes, a cherished dream. But let’s be honest, that dream machine often comes with a price tag that makes us pause. That’s where the magic of a two-wheeler loan steps in.

You see, buying a bike or a scooter outright with cash isn’t always feasible for everyone, and that’s perfectly okay. What’s not okay is letting that dream gather dust. This isn’t just about getting a loan; it’s about understanding how to smartly leverage bike finance to make your aspiration a reality without breaking the bank. I’ve seen countless folks navigate this path, and the common thread? A little knowledge goes a long way. So, let’s peel back the layers and truly understand what it takes to get you on that saddle.

The Dream Machine | Why a Two-Wheeler Loan Matters

Think about it. The daily commute, the quick grocery runs, visiting family across town, or even those spontaneous weekend getaways – a two-wheeler offers unparalleled convenience and flexibility. In India, where public transport might not always reach every nook and cranny, and where roads can be unpredictable, a personal two-wheeler is often a necessity disguised as a luxury. But the upfront cost, especially for some of the more premium models, can be substantial. This is precisely why two-wheeler loan options have become such a lifeline.

It’s not just about affordability; it’s about financial planning. Instead of depleting your savings, a loan allows you to spread the cost over manageable monthly installments, known as EMIs. This frees up your capital for other essential investments or emergencies. It’s a strategic financial move, especially for young professionals, students, or anyone looking to upgrade their ride without a significant one-time outflow. What truly fascinates me is how these loans empower individuals, turning a distant desire into a tangible possession. It’s a tool for personal mobility, yes, but also a gateway to greater opportunities and a touch of everyday freedom. It’s about not just owning a bike, but owning your journey.

Navigating the Loan Labyrinth | Eligibility & Documents

Alright, so you’re convinced. The dream is real, and a two-wheeler loan is your chosen path. Now comes the nitty-gritty: who qualifies and what paperwork do you need? This is where many people get a little intimidated, but honestly, it’s not as complex as it seems if you know the ropes.

Understanding Loan Eligibility Criteria

Every lender has their own set of criteria, but there are common threads. Typically, you’ll need to be:

- An Indian citizen.

- Between 18 to 65 years of age (this can vary slightly).

- Either salaried, self-employed, or a professional with a stable income source.

- Have a decent credit score. This is crucial! A good score (usually 700+) signals to lenders that you are a responsible borrower. If your score is on the lower side, don’t despair; some lenders might still offer a loan but possibly at higher interest rates or with a larger down payment.

The minimum income requirement is also a factor, ensuring you can comfortably repay the EMIs. Lenders want to see stability. A common mistake I see people make is not checking their credit score before applying. It’s like going to war without scouting the terrain!

The Paper Trail | Documents Required for Bike Loan

Gathering your documents proactively can significantly speed up your loan application process . Here’s a general checklist:

- Identity Proof: Aadhar card, PAN card, Passport, Driving License.

- Address Proof: Aadhar card, Passport, Utility bills (electricity, phone), Rent agreement.

- Income Proof:

- For Salaried Individuals: Latest 3 months’ salary slips, Form 16, Bank statements (for the last 6 months) showing salary credits.

- For Self-Employed Individuals: Latest ITR (Income Tax Return) with income computation, Bank statements (for the last 6-12 months), Business proof.

- Bank Statements: Usually for the last 3-6 months.

- Proforma Invoice/Quotation from the dealer for the two-wheeler you intend to purchase.

- Passport-sized photographs.

It sounds like a lot, right? But most of these are documents you likely already have. The key is to have them organized and ready. Sometimes, having a co-applicant can also bolster your chances, especially if you’re new to credit or have a fluctuating income. Remember, the clearer you make your financial picture, the smoother the process will be. For more insights on various vehicle financing options, you might find this resource helpful:Vehicle Loan Category.

Demystifying the Numbers | Interest Rates & EMIs

Once you’ve got your eligibility and documents sorted, the next big question is usually about money – specifically, interest rates and your monthly EMI options . These are the twin pillars that determine the true cost and affordability of your two-wheeler loan .

Understanding Interest Rates for Two-Wheelers

Interest is the cost of borrowing money. For two-wheeler finance , interest rates can be fixed or floating, though most are fixed. They vary from lender to lender and depend on several factors:

- Your Credit Score: A higher score usually translates to a lower interest rate.

- Loan Amount & Tenure: Sometimes, larger loans or longer tenures might have slightly different rates.

- Lender’s Policies: Each bank or NBFC has its own internal lending policies.

- Economic Factors: Broader market conditions and RBI policies can also influence rates.

Don’t just jump at the lowest advertised rate. Always read the fine print. Look for hidden charges like processing fees, foreclosure charges, or late payment penalties. Transparency is key here. As per general financial guidelines (you can check resources like Wikipedia for general loan principles:Loan on Wikipedia), understanding the APR (Annual Percentage Rate) gives you a clearer picture of the total cost.

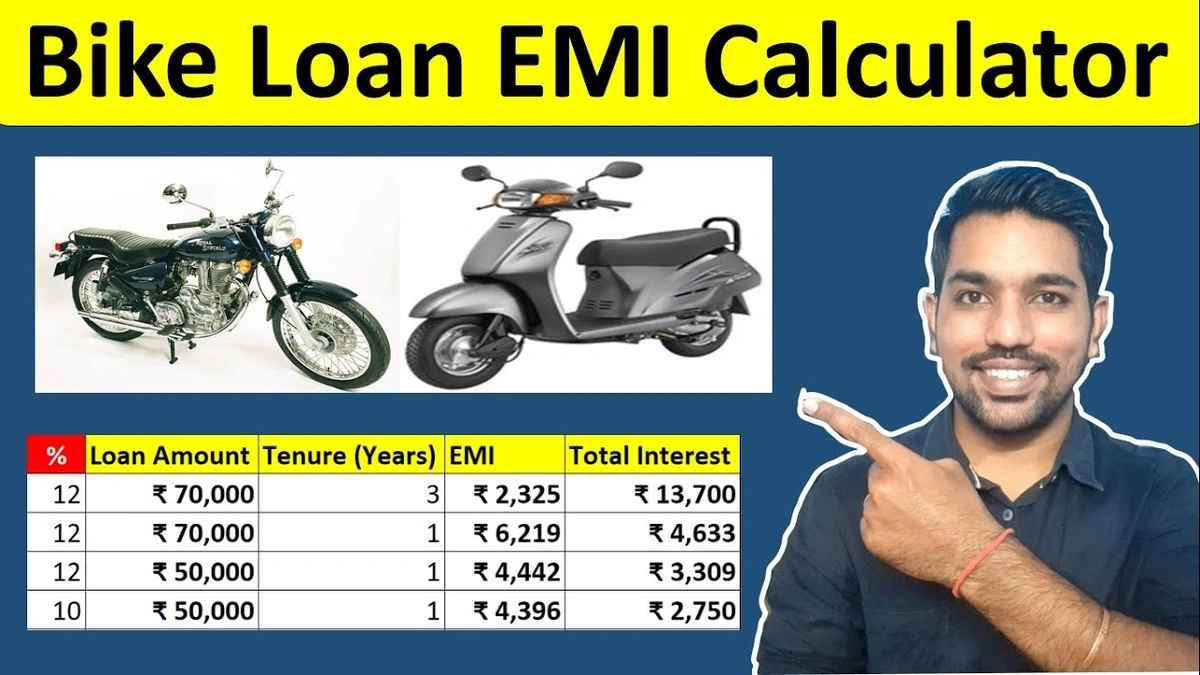

Calculating Your EMI for Two-Wheeler Loan

EMI stands for Equated Monthly Installment. It’s the fixed amount you pay back to the lender each month until the loan is fully repaid. Your EMI depends on three things:

- P (Principal): The actual loan amount.

- R (Rate of Interest): The annual interest rate.

- N (Number of Installments): The loan tenure in months.

Many banks and financial websites offer an easy-to-use two-wheeler loan calculator . Just punch in the numbers, and it will give you an estimated EMI. My advice? Play around with the calculator. See how different loan amounts, interest rates, and tenures impact your EMI. A longer tenure means lower EMIs but higher overall interest paid. A shorter tenure means higher EMIs but less interest. It’s a balancing act to find what fits your budget comfortably. Don’t overstretch yourself! The ideal EMI should not strain your monthly budget.

Your Application Journey | From Online Click to Key in Hand

So, you’ve done your homework, gathered your documents, and have a clear idea of your budget. What’s next? The actual application! In today’s digital age, applying for an online two-wheeler loan is incredibly convenient.

The Modern Way | Online Two-Wheeler Loan Application

Most banks and financial institutions now offer a seamless online application process. You can visit their websites or use their mobile apps. Here’s a typical flow:

- Fill out the Application Form: Provide personal, financial, and employment details.

- Upload Documents: Scan and upload the required proofs (Identity, Address, Income, etc.).

- Verification: The lender will verify your documents and conduct a credit check. They might call you for further clarification.

- Loan Approval & Disbursement: Once approved, the loan amount is usually disbursed directly to the two-wheeler dealer.

The speed of this process can vary, but often, an online two-wheeler loan can be approved and disbursed within a few days, sometimes even faster if all your documents are in order and your credit profile is strong. While convenience is great, always ensure you’re applying through official and secure channels. phishing scams are unfortunately a reality, so double-check URLs and security certificates.

The Role of Down Payment for Bike Loan

While a loan covers a significant portion of the bike’s cost, most lenders require a down payment . This is the initial lump sum you pay out of your own pocket. Typically, it ranges from 10% to 30% of the vehicle’s on-road price. A higher down payment can reduce your principal loan amount, thereby lowering your EMIs and the total interest paid over the loan tenure. It also often makes your application more attractive to lenders, potentially securing you better terms.

Beyond the Loan | Smart Ownership Tips

Getting the loan is just the first step; smart ownership is about what comes after. Once you have your two-wheeler, managing your loan and maintaining your vehicle intelligently can save you money and headaches in the long run.

- Timely EMI Payments: This is non-negotiable. Missing EMIs or making late payments severely impacts your credit score and incurs penalties. Set up auto-debit if possible.

- Insurance is a Must: Beyond the mandatory third-party insurance, consider comprehensive insurance. It protects your investment against theft, accidents, and natural calamities.

- Regular Servicing: Keep your two-wheeler in top condition. Regular maintenance not only ensures safety but also extends the life of your vehicle and maintains its resale value.

- Consider Prepayment: If you find yourself with extra funds, consider making partial or full prepayments. This reduces your principal and thus the total interest you pay. However, check for any prepayment penalties first.

Remember, a two-wheeler loan is a commitment. Treat it with respect, and it will serve you well. It’s not just about acquiring an asset; it’s about responsibly managing your finances to enhance your life. For a deeper dive into managing your finances and understanding various personal borrowing options, you might want to explore articles onPersonal Loancategories, as many principles overlap.

Frequently Asked Questions About Two-Wheeler Loans

What is the typical down payment for a bike loan?

The typical down payment for a bike loan usually ranges from 10% to 30% of the vehicle’s on-road price. A higher down payment can lead to lower EMIs and reduced interest costs over the loan tenure.

How long does it take to get a two-wheeler loan approved?

The approval and disbursement time for a two-wheeler loan can vary. For online applications with all documents in order and a good credit score, it can be as quick as a few hours to 2-3 business days. Traditional applications might take longer, typically 3-7 days.

Can I get a two-wheeler loan without a good credit score?

While a good credit score (700+) significantly improves your chances and secures better terms, it’s not impossible to get a loan with a lower score. However, lenders might offer the loan at a higher interest rate, require a larger down payment, or ask for a co-applicant to mitigate their risk.

Is it better to opt for a longer or shorter loan tenure?

A shorter loan tenure means higher monthly EMIs but results in paying less total interest over the life of the loan. A longer tenure offers lower EMIs, making it more affordable monthly, but you end up paying more interest in total. The best option depends on your monthly budget and long-term financial goals.

Can I prepay my two-wheeler loan?

Yes, most lenders allow you to prepay your two-wheeler loan, either partially or fully, before the tenure ends. However, it’s important to check if there are any prepayment or foreclosure charges associated with this, as these can sometimes negate the benefit of saving on interest.

The journey to owning your two-wheeler doesn’t have to be complicated. With the right information, a dash of planning, and a clear understanding of the two-wheeler loan process, you can transform that dream into a tangible reality. So go ahead, dream big, plan smart, and soon, you’ll be cruising down your chosen path with confidence and joy. Your road to freedom awaits!