Alright, let’s talk about something that can either save you a ton of cash or quietly drain your wallet: used car loan interest rates USA . If you’re eyeing a pre-loved set of wheels in America, you’ve probably already realized that the sticker price is just one piece of the puzzle. The real game-changer? That pesky interest rate. And here’s the thing: it’s not just a number on a screen; it’s a reflection of market dynamics, your financial standing, and frankly, how well you play your cards.

I get it, the world of auto loan rates can feel like a labyrinth. You see headlines about the Federal Reserve, you hear whispers about inflation, and suddenly, that dream car feels a little further away. But what if I told you that with a bit of savvy, some insider knowledge, and a clear strategy, you can absolutely secure a fantastic deal? This isn’t about magic; it’s about understanding the “why” behind the numbers and mastering the “how” of getting approved. Let’s dive deep, shall we?

Why Are Used Car Loan Interest Rates So Tricky Right Now?

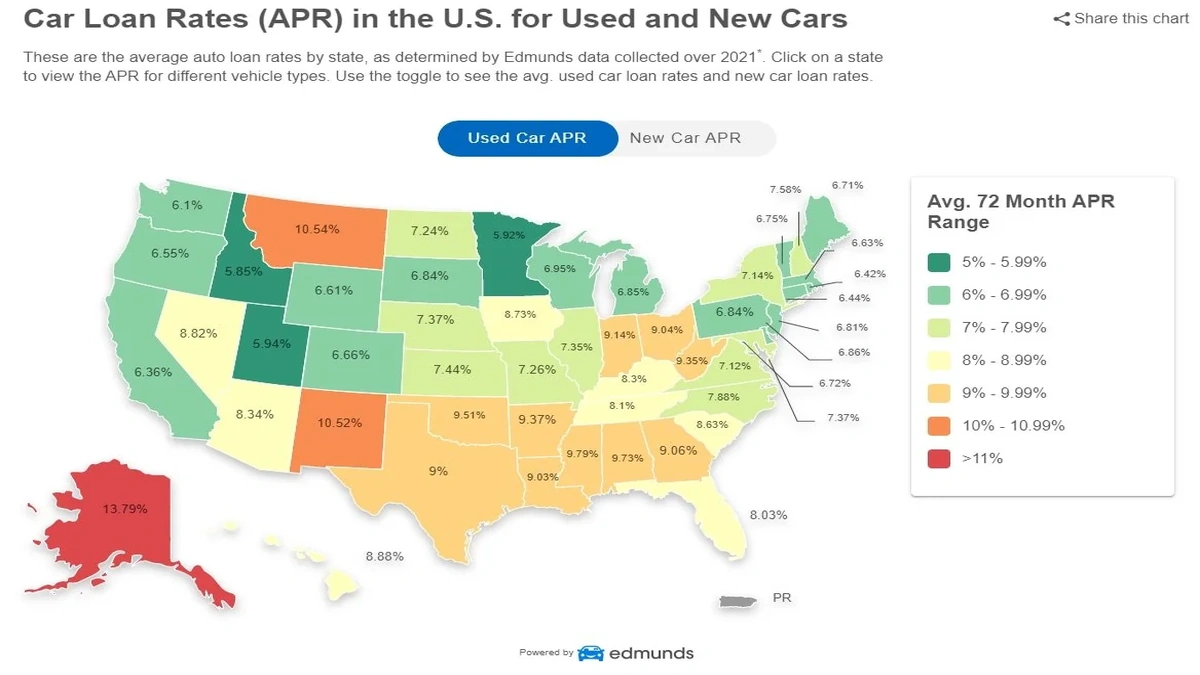

You might be wondering, “Why does it feel like used car loans are more complex than ever?” Good question! It’s not just you. Several factors are creating a perfect storm in the market. First off, the overall economic climate plays a massive role. When the Federal Reserve adjusts its benchmark rates, it has a ripple effect across all lending, includingcar financing. Higher federal rates often translate to higher lending rates for consumers. What fascinates me is how quickly these macro trends impact our everyday purchases.

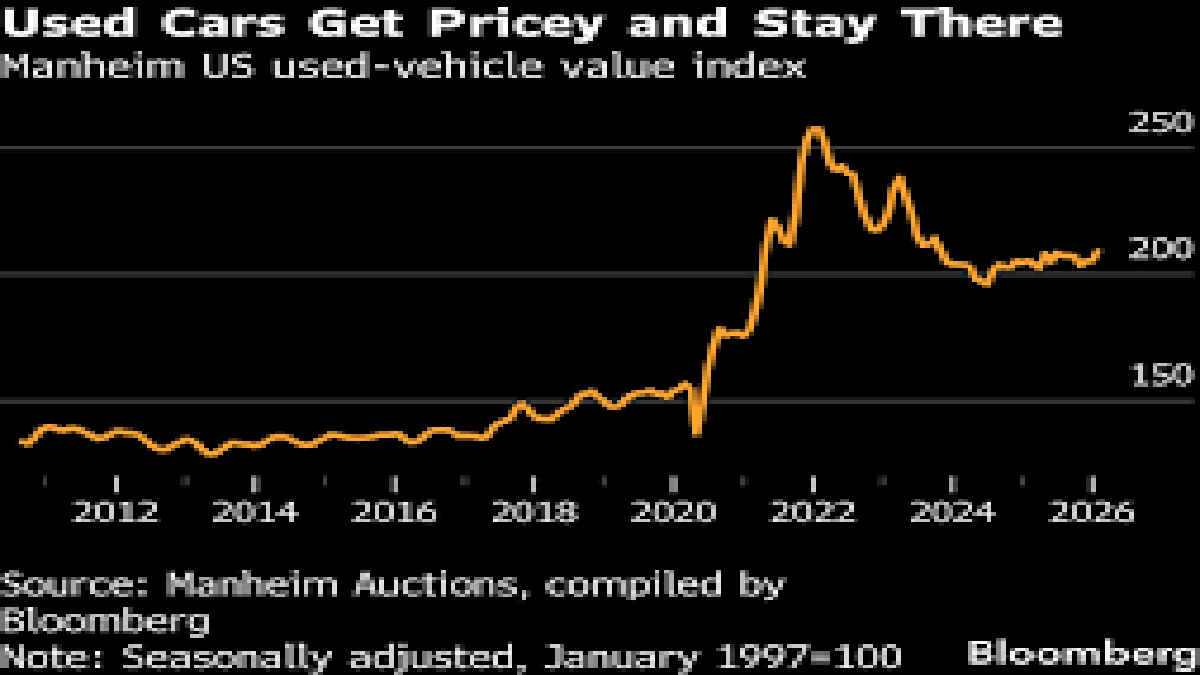

Then there’s the supply and demand for used vehicles themselves. Post-pandemic, we saw an unprecedented surge in used car prices due to new car production issues. While things have stabilized a bit, the residual effect means lenders might perceive used cars, especially older models, as slightly riskier assets. This translates into potentially higher used car loan interest rates compared to new car loans, simply because the depreciation curve is different, and the collateral value might be less predictable for the lender over the loan term. Understanding this hidden context is crucial for anyone looking into financing a used car .

Your Credit Score | The Unsung Hero (or Villain) of Your Loan Application

Let’s be brutally honest for a moment: your credit score is probably the single biggest determinant of the interest rate you’ll be offered. It’s your financial report card, telling lenders how responsible you’ve been with borrowing money in the past. A high score (think 700+) signals trustworthiness, often unlocking the lowest APR (Annual Percentage Rate) available. A lower score, on the other hand, means lenders see more risk, and they’ll compensate for that risk by charging you a higher rate.

I’ve seen countless people make this mistake: they don’t check their credit score before they start shopping for a car. Don’t be that person! Get a copy of your credit report from one of the three major bureaus (Experian, Equifax, TransUnion) and review it for errors. Even a small mistake can ding your score and cost you hundreds, if not thousands, over the life of your loan. Knowing your score empowers you to negotiate and understand what kind of rates you genuinely qualify for. It’s foundational to navigating the loan approval process successfully.

Mastering the “How” | Steps to Secure the Best Used Car Loan Rates

1. Get Pre-Approved (Seriously, Do This!)

This is my number one piece of advice. Don’t walk into a dealership without a pre-approval for used cars in hand. Why? Because it gives you immense leverage. When you’re pre-approved by a bank or credit union, you know exactly what rate you qualify for and how much you can borrow. This transforms your car shopping experience. Instead of negotiating a car price and a loan rate simultaneously (a dealer’s dream scenario), you can focus solely on the car’s price, knowing your financing is already sorted. It’s like having a secret weapon.

2. Shop Around for Lenders (Beyond the Dealership)

While dealership financing can be convenient, it’s rarely the best option. Banks, credit unions, and online lenders often offer more competitive auto loan rates . Credit unions, in particular, are known for their customer-friendly rates because they’re member-owned. Don’t just take the first offer! Apply to a few different institutions within a short window (typically 14-45 days, depending on the credit model) to minimize the impact on your credit score. This allows you to compare offers side-by-side and pick the one with the lowest APR and most favorable loan terms .

3. Consider Your Down Payment & Loan Term

A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over time. It’s simple math, but often overlooked. Similarly, while a longer loan term (e.g., 72 months) might offer lower monthly payments, you’ll almost always pay significantly more in total interest. Shorter terms (36 or 48 months) are often ideal if your budget allows, drastically cutting down the overall cost of your used car loan interest rates USA .

4. Understand All Fees & The Total Cost

Always look beyond the interest rate. Are there origination fees? Prepayment penalties? Some loans, like secured loans (e.g., a gold loan where the asset acts as collateral), might have different fee structures compared to an unsecured personal loan. For example, understanding how aninstant gold loan online approvalworks involves similar principles of assessing fees and overall costs, even if the collateral is different. The same goes for understanding the step-by-step process ofhow a gold loan works– transparency in fees is key across all lending products. Always ask for the total cost of the loan, not just the monthly payment.

When Refinancing Car Loans Makes Sense

What if you’ve already got a used car loan, and those interest rates are giving you buyer’s remorse? Don’t despair! Refinancing car loans is a powerful tool that many people overlook. If your credit score has improved since you first took out the loan, or if market rates have dropped significantly, you might be able to secure a lower interest rate, reduce your monthly car payments , or even shorten your loan term. It’s essentially taking out a new loan to pay off your old one, but hopefully, with better terms. This is a particularly smart move if you initially financed through a dealership and suspect you weren’t offered the best rate.

FAQs

What is a good interest rate for a used car loan in the USA?

A “good” interest rate for a used car loan in the USA typically falls between 4% and 7% for borrowers with excellent credit (720+ FICO score). However, rates vary significantly based on your credit score, the loan term, the lender, and current market conditions. It’s crucial to shop around to find the best rate you qualify for.

Does a down payment affect my used car loan interest rate?

While a down payment primarily reduces the amount you need to borrow and thus your monthly car payments, it can indirectly influence your interest rate. Lenders often view a larger down payment as a sign of financial stability and reduced risk, which might make them more inclined to offer you a slightly lower interest rate.

Can I get a used car loan with bad credit?

Yes, it’s possible to get a used car loan with bad credit, but be prepared for significantly higher interest rates. Lenders offering “subprime” loans charge more to compensate for the increased risk. Focus on improving your credit score before applying, or consider a co-signer to get a better rate.

How long can I finance a used car for?

Common loan terms for used cars range from 36 to 72 months. While longer terms offer lower monthly payments, they also mean you’ll pay more in total interest over the life of the loan. Most experts recommend keeping the loan term as short as your budget comfortably allows to minimize overall costs.

Is pre-approval for a used car loan worth it?

Absolutely! Getting pre-approval for used cars is highly recommended. It provides you with a clear budget, an actual interest rate you qualify for, and significant negotiation power at the dealership. It separates the financing from the car purchase, making the process much more transparent and putting you in control.

What’s the difference between APR and interest rate?

The interest rate is the cost of borrowing money, expressed as a percentage. The APR (Annual Percentage Rate) includes the interest rate PLUS any additional fees associated with the loan, such as administrative fees. It gives you a more accurate picture of the total annual cost of your loan, so always compare APRs, not just interest rates.

So, there you have it. Navigating used car loan interest rates USA doesn’t have to be a bewildering experience. By understanding the “why” the market forces and your credit’s influence and by diligently applying the “how” getting pre-approved, shopping smart, and optimizing your loan terms you’re not just buying a car; you’re making a smart financial decision. Go forth, get that dream car, and do it with confidence, knowing you’ve got the best possible deal. Your wallet will thank you!